The Annual Enrollment Period (AEP) for Medicare Advantage (MA) plans (Part C) is almost here! If you have an Advantage plan and you’d like to change to a traditional Medicare Supplement plan, you can apply during the upcoming AEP, which is from October 15th through December 7th, for an effective date of January 1st, 2016.

The Annual Enrollment Period (AEP) for Medicare Advantage (MA) plans (Part C) is almost here! If you have an Advantage plan and you’d like to change to a traditional Medicare Supplement plan, you can apply during the upcoming AEP, which is from October 15th through December 7th, for an effective date of January 1st, 2016.

If you have an Advantage plan or a Prescription Drug Plan (PDP), this is the one time of year to make changes to your health and/or prescription drug plans for the following year. To make these changes, the plan has to receive your enrollment request (application) no later than December 7th. If you stay with the same plan that you had, any changes to coverage, benefits, or costs for the new year will also begin on January 1st.

What is the Annual Notice of Change (ANOC)

If you have an Advantage plan, your plan will send you an “Annual Notice of Change” (ANOC) each fall. The ANOC includes any changes in coverage, costs, provider networks, or service areas that will be effective in January. These are usually mailed out in September by your Advantage plan. After you receive your notice, review any changes to decide whether the plan will continue to meet your needs during the following year. If you don’t receive this important notice, contact your Advantage plan and request that they send it to you.

If you have an Advantage plan, your plan will send you an “Annual Notice of Change” (ANOC) each fall. The ANOC includes any changes in coverage, costs, provider networks, or service areas that will be effective in January. These are usually mailed out in September by your Advantage plan. After you receive your notice, review any changes to decide whether the plan will continue to meet your needs during the following year. If you don’t receive this important notice, contact your Advantage plan and request that they send it to you.

IMPORTANT: If you have health conditions that may prevent you from meeting the underwriting requirements for a Medicare Supplement, the ANOC may qualify you for one of the “guaranteed issue” situations listed below.

Minimum Health Requirements for a Medicare Supplement

To apply for a Medicare Supplement during the AEP, you must complete a Medicare Supplement application, which includes a section with health questions. If you have serious health issues, there is a good chance that your application will be turned down. However, there are certain “guaranteed issue” situations that you may qualify for. This means that you will not have to answer any of the health questions on the application, and you cannot be turned down!

In the “Eligibility for Guaranteed Issue In California” section below, there are nine situations that would guarantee you the right to change your Advantage plan to a Medicare Supplement plan, REGARDLESS OF YOUR HEALTH, without answering any health questions on the application!

Carefully check the ANOC. If your Medicare Advantage plan has increased your premium or co-payments by 15% or more, reduced your benefits, or terminated its relationship with your medical provider who was treating you, YOU PROBABLY QUALIFY FOR A GUARANTEED ISSUE MEDICARE SUPPLEMENT PLAN!

Guaranteed Issue Rights

Guaranteed issue rights are rights you have in certain situations when insurance companies MUST offer you certain Medicare Supplement policies (plans A, B, C, F, K, or L). In these situations, an insurance company:

- Must sell you a Medicare Supplement policy

- Must cover all your pre-existing health conditions

- Can’t charge you more for a Medicare Supplement policy because of past or present health problems

In most cases, you have a guaranteed issue right when you have other health coverage that changes in some way, such as when you lose the other health care coverage. In other cases, you have a “trial right” to try an Advantage plan and still buy a Medicare Supplement policy if you change your mind.

Eligibility for Guaranteed Issue In California

In California, you would qualify for a guaranteed issue Medicare Supplement for any of the following situations:

- Has your employer-sponsored retiree plan that is supplementing Medicare involuntarily terminated?

- Has your employer-sponsored retiree plan stopped providing Medicare supplement benefits or the Medicare Part B 20% coinsurance for services?

- Have you lost eligibility for an employer-sponsored retiree plan due to divorce or death of a spouse or family member?

- Has your Medicare Advantage plan increased your premium or co-payments by 15% or more, reduced your benefits, or terminated its relationship with your medical provider who was treating you?

- Have you moved out of the area of your MA plan or Program for All-Inclusive Care for the Elderly (PACE) organization?

- Has your MA plan, Medicare SELECT Plan, PACE provider or any other health plan under contract with Medicare: (a) committed fraud; (b) ended or lost its contract with Medicare; (c) misrepresented the plan you bought, or (d) failed to meet its contractual obligations to Medicare beneficiaries, as determined by the federal government?

- Did you join a MA plan or PACE organization when you first became eligible for Medicare at age 65, and you want to switch to a Medicare Supplement policy during your first 12 months in the MA plan or PACE organization?

- Have you switched from a Medicare Supplement policy to a MA plan, PACE organization, Medicare SELECT plan, or any other health care organization contracting with Medicare, for the first time since becoming eligible for Medicare within the past 12 months?

- Has your MA plan left your area, and if so, did your MA plan benefits end within the past 123 days?

Purchasing a Medicare Supplement Insurance Policy if You’ve Lost Your Health Care Coverage

If you believe that you have a guaranteed issue right to purchase a Medicare Supplement policy, make sure you keep the following items:

- A copy of any letters, notices, emails, and/or claim denials that have your name on them as proof of your coverage being terminated.

- The postmarked envelope these papers come in as proof of when it was mailed.

- You may need to send a copy of some or all of these papers with your Medicare Supplement application to prove you have a guaranteed issue right.

- If you have a Medicare Advantage Plan but you’re planning to return to Original Medicare, you can apply for a Medicare Supplement policy before your coverage ends. The Medicare Supplement insurer can sell it to you as long as you’re leaving the plan. Ask that the new policy take effect no later than when your Medicare Advantage enrollment ends, so you’ll have continuous coverage.

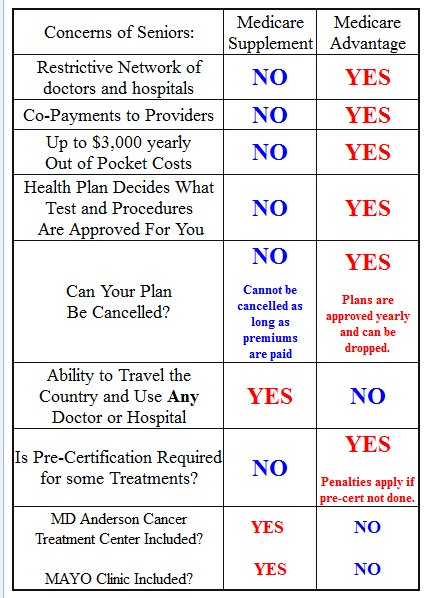

Which is Better, a Medicare Supplement or an Advantage Plan?

This topic is big enough to have its own blog! Personally, I strongly prefer Medicare Supplements over Advantage plans because you can go to ANY doctor or hospital in the US as long as they accept Medicare, and most of them do. With an Advantage plan, you are limited to their local networks of doctors and hospitals, and that is a major disadvantage. Also, a lot of people seem to think that Advantage plans cost less than Medicare Supplements, but if you are every hospitalized or develop a serious medical condition, you will be spending thousands of dollars on co-payments and deductibles with your Advantage plan.

Here are some pros and cons when comparing Medicare Supplements to Advantage plans.

For the reasons mentioned above, I would recommend Medicare Supplements over Advantage plans. If you are relatively healthy, an Advantage plan may be okay. But if you later develop serious health conditions, you’ll wish you had a Medicare Supplement because you should have the freedom to go to the best doctors, hospitals, specialists, and facilities ANYWHERE in the United States!

For the reasons mentioned above, I would recommend Medicare Supplements over Advantage plans. If you are relatively healthy, an Advantage plan may be okay. But if you later develop serious health conditions, you’ll wish you had a Medicare Supplement because you should have the freedom to go to the best doctors, hospitals, specialists, and facilities ANYWHERE in the United States!

If you (or someone you know) have an Advantage plan and you have any questions or would like to find out more about Medicare Supplement plans, please contact me at Ron@RonLewisInsurance.com. As an independent agent, I work with ALL the major insurance carriers in California, Washington, Nevada, and Arizona, and I’ll shop around for you to get you the best rates.