The Annual Election Period (AEP) is from October 15th through December 7th each year. During this annual open enrollment period, you can sign up for or change your Medicare Advantage (MA) plan or your Prescription Drug Plan (PDP). Medicare Advantage and prescription drug plans are annual contracts, and they can change from year to year. Therefore, you should shop around and compare plans every year.

NOTE: If you have a Medicare Supplement, the AEP does not apply to you unless you want to enroll in or change your PDP.

If you have an MA plan and you want to change to a different MA plan, or if you want to leave your MA plan and switch back to Original Medicare, Part A (Hospital insurance) and Part B (Medical insurance), you would normally do so during the AEP. The new coverage will begin on January 1st of the following year. In most cases, you must stay enrolled in your MA plan for the calendar year beginning in January or on the date your coverage begins. However, in certain situations, you may be able to join, switch, or drop an MA plan during a Special Enrollment Period (SEP), such as if you move out of your plan’s service area, etc.

Pros and Cons – Medicare Supplements Versus Medicare Advantage Plans

When it comes to Medicare Advantage (MA) plans, I’m going to be totally honest and admit to you that I am biased because I don’t like them! Unless you can’t afford to pay the monthly premium for a Medicare Supplement (aka Medigap), I would NEVER recommend or advise someone to give up their Original Medicare rights (Part A and Part B) and sign up for an MA plan!

If you currently have an MA plan, or if you are thinking about signing up for one, I would strongly recommend that you read this article first so that you can make an “informed decision” about whether an MA plan is right for you and in your best interest.

There are pros and cons to each, but the benefits of having a Medicare Supplement plan far outweigh the benefits of having an MA plan. Please click here for a detailed comparison between Original Medicare and Medicare Advantage plans.

MA Plan Advantages

Here are some of the benefits of having an MA plan:

- MA premiums can be very low, and some plans have no monthly premiums at all.

- Some MA plans include Medicare prescription drug coverage (Part D).

- Maximum out-of-pocket (OOP) costs are limited. Plans vary, but in 2025, the most you can pay for in-network OOP costs is $9,350 per calendar year. If you go out of network, you would normally pay all costs! (I wouldn’t really call this a benefit since $9,350 is a lot of money, and the most you would pay in OOP costs with a Plan G Medicare Supplement is the Medicare Part B deductible, which is currently $240 per calendar year in 2024! The Medicare Part B deductible for 2025 is projected to be $257. However, the Centers for Medicare & Medicaid Services (CMS) will not finalize the deductible until fall 2024.)

- Some MA plans offer additional benefits such as vision, hearing, dental, and other health and wellness programs. (Some Medicare Supplement plans also offer additional benefits such as free gym memberships, vision, and hearing aid benefits.)

Medicare Supplement Plan Advantages

Here are some of the benefits of having a Medicare Supplement plan:

- You have much more FREEDOM of choice with a Medicare Supplement than you do with an MA plan because you can go to ANY doctor, hospital, specialist, care facility, etc. in the United States as long as they accept Medicare, and most do, about 93%. (You can’t do that with an MA plan.)

- You have much for financial stability with a Medicare Supplement than an MA plan because there are no unexpected expenses for deductibles, co-payments, hospitalizations, surgeries, chemotherapy, etc.

- With a Plan G Medicare Supplement, other than your premiums, your maximum OOP cost in the 2025 calendar year will be no more than the Part B deductible, which is currently projected to be around $257. With an MA plan, your in-network maximum OOP “in-network” costs can be as high as $9,350! If you go out of network, your costs can be significantly higher.

NOTE: The Medicare Part B deductible is payable only one time per calendar year. If you’ve already met that deductible, you won’t have any other costs for Medicare-approved charges for the rest of the year.

- You are not limited to a specific geographic region or a restrictive network of doctors, hospitals, specialists, care facilities, etc. like you are with an MA plan. Most MA plans are HMO’s and you will normally pay all costs if you go out of network.

- With a Medicare Supplement, you can go directly to the specialist of your choice, ANYWHERE in the United States, as long as they accept Medicare. Most MA plans require you to go through a primary care doctor first and get permission to see a specialist within the local, geographic network.

- Unlike MA plans, there are no HMO or PPO plans or networks with Medicare Supplements. You can go to any doctor or specialist in the US as long as they accept Medicare.

- If you want to go to a renowned treatment center such as the MD Anderson Cancer Treatment Center in Texas, you can do so with any Medicare Supplement, as long as they accept Medicare. You can’t do that with most MA plans.

- If you move to another part of the country, you can keep your Medicare Supplement, but you cannot keep your MA plan if you move out of your network.

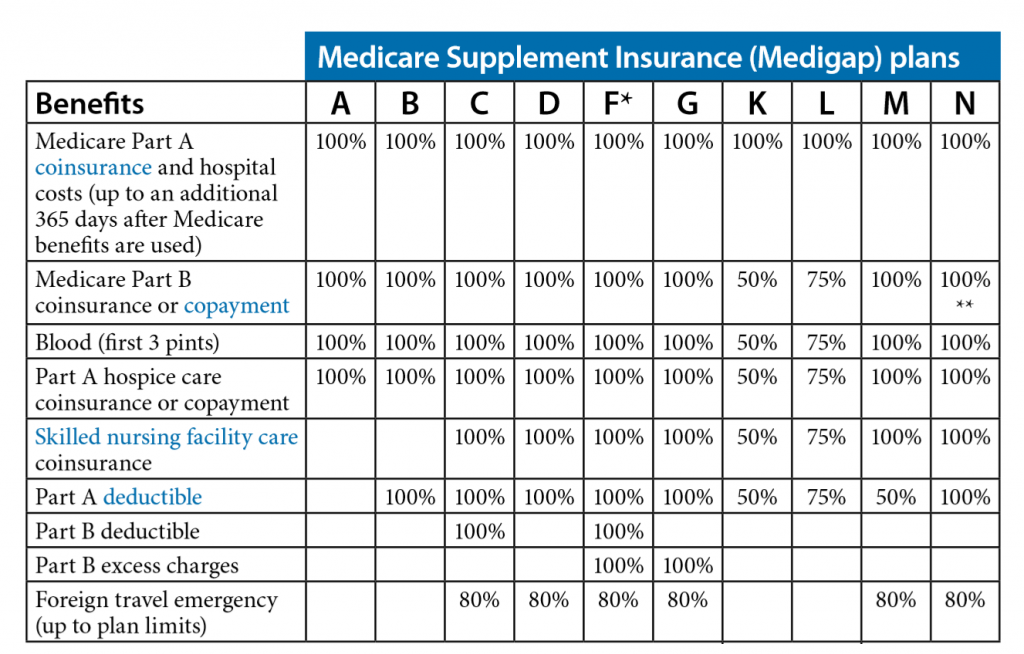

- There are only 10 “standardized” Medicare Supplement plans to choose from, (Plan A through Plan N). Since Medicare Supplements are standardized, the coverage and benefits for every Plan G, etc. is exactly the same with every insurance carrier, so it’s much easier to shop around and compare “apples with apples.” MA plans are not standardized, and the co-payments, deductibles, out of pocket costs, etc. vary between MA plans, and they change every year making them unnecessarily complicated and confusing.

- A Medicare Supplement plan cannot be cancelled as long as you pay your premiums. MA plans are annual contracts, and they can be cancelled or benefits changed at the end of each calendar year.

- There is no Annual Election Period (AEP) for Medicare Supplements, and you don’t have to shop around every year and make sure that your coverage, co-payments, co-insurance, deductibles, and benefits haven’t changed since the previous year. If there are any Medicare changes from one calendar year to the next, your Medicare Supplement will automatically pay the difference.

- Medicare Supplements are “portable” meaning that you can keep them and take them with you if you travel to another state or if you move to another state, and your Medicare Supplement cannot be cancelled for leaving your “service area.” With most MA plans, if you travel outside of the MA plan’s service area for more than six months, you could be dis-enrolled from the plan.

- With a Plan G Medicare Supplement, there are no co-payments when you go to the doctor. With most MA plans, you have to pay co-payments every time you see a doctor.

- You can switch Medicare Supplement plans or Medicare insurance carriers any time of the year as long as you meet minimum health and underwriting requirements. With an MA plan, you can only join or leave an MA plan during the AEP or a SEP. Otherwise, you are locked into your MA plan for the entire calendar year.

NOTE: In California, there is a law called the California Birthday Rule. Under this law, if you have a Medicare Supplement, you can change it every year during the 60 days following your birthday to any other Medicare Supplement plan with “equal or fewer” benefits. For example, if you have Plan G, you can switch to Plan G with any other insurance carrier, regardless of your health. If you have Plan G, you can also switch to Plan N because Plan N has fewer benefits than Plan G, etc. Under the birthday rule, you just can’t switch from a plan with fewer benefits to greater benefits.

As you can see from the facts mentioned above, the benefits of having a Medicare Supplement far outweigh the benefits of having a Medicare Advantage plan.

Are Some Medicare Advantage Plans Really Free?

Because some MA plans have very low monthly premiums or no monthly premiums at all, some unscrupulous individuals promote them as “FREE” Medicare insurance plans, which is inaccurate, misleading, and, in my opinion, unethical. During the AEP, there are a lot of commercials for MA plans on TV. If you listen carefully, the one thing you’ll NEVER hear them mention is the maximum out-of-pocket costs for those plans. In 2025, in-network OOP costs can be as high as $9,350, and if you go out of network, you can pay significantly more!

Also, regardless of whether you have an MA plan or a Medicare Supplement plan, you still have to pay the monthly Medicare Part B premium, which is currently $174.70 per month for most people in 2024. The Medicare Part B premium in 2025 hasn’t been released yet, but it is estimated to be around $185.00 per month.

You Can Always Get a Medicare Advantage Plan But You Can’t Always Get a Medicare Supplement Plan

MA plans are adequate as long as you are healthy, but if your health should change and you develop a serious illness, you will wish that you had a Medicare Supplement instead of an MA plan because you will have much more freedom of choice and control over your health care with a Medicare Supplement!

Original Medicare (Part A and B) only cover about 80% of medical and hospital costs and Medicare Supplements pick up most of the remaining 20%. During the AEP, you can always switch from a Medicare Supplement to an MA plan, regardless of your health, and you can always switch from an MA plan back to Original Medicare (Part A and Part B), regardless of your health. However, if you switch back from an MA plan to Original Medicare during the AEP, there is no guarantee that you can get a Medicare Supplement as you must be in good health, answer health questions, and be medically underwritten to be approved. If you have any serious health issues, more than likely, you won’t be able to get a Medicare Supplement.

NOTE: There are some situations where you can switch from an MA plan to a Medicare Supplement as a “guaranteed issue” without answering any health questions or going through medical underwriting. If you are in this situation, please let me know.

Also, if you are in the first year of your MA plan, you are guaranteed the right to switch back to a Medicare Supplement during the first 12 months. This is called a trial right. The trial period gives you a year to try an MA plan and see if it’s right for you. If you decide it’s not, you are guaranteed the right to switch back to original Medicare (Parts A and B) and purchase a Medicare Supplement plan.

The Maximum Out of Pocket Cost for MA Plans Can Be Twice As Much As You Think

Depending on which MA plan you have, the most you would pay for in-network out-of-pocket (OOP) costs in 2025 is $9,350 per calendar year! If you go outside of your plan’s network, you will pay even more than that!

Now suppose that you get really sick and need expensive treatment in the second half of the year. You could end up paying up to $9,350 (or whatever your plan’s maximum OOP cost is) by the end of the calendar year, but your OOP maximum zeros out in January, and it starts all over again! You could potentially end up paying your OOP TWICE in a 12-month period!

Conclusion

If you have an MA plan, you give up your Original Medicare (Part A and Part B) rights and you compromise your freedom of choice to go to the best doctors, specialists, hospitals, care facilities, etc. throughout the United States. Unless you are impoverished and can’t afford to pay the monthly premium for a Medicare Supplement, I would never recommend an MA plan to a friend or family member as you are always better off with a Medicare Supplement.

I’m an independent insurance agent, not a captive agent, and I work with most of the major insurance carriers. I shop around for my clients, every year, and I will shop around for you too! If you have any questions or if you have an MA plan and would like for me to help you switch to a Medicare Supplement plan, please let me know! And if you have a Medicare Supplement, I’m happy to shop around for you to save you money on your premiums!

There’s no such thing as free Medicare insurance! As the old expression goes… “You get what you pay for!”

If you liked this blog and found it informative, please click the “Like” button, and please send me your questions, comments, or feedback! And please feel free to share this article with your friends!

Thank you!

Ron Lewis

Ron@RonLewisInsurance.com

www.MedigapShopper.com

(760) 525-5769 – Cell

(866) 718-1600 – Toll-free