Many seniors in California do not realize they have a special opportunity each year to change their Medicare Supplement plan without answering health questions. This opportunity is called the California Birthday Rule and it can be a valuable way to adjust coverage or reduce premiums if your needs have changed. Even if you are happy with your current plan, understanding the birthday rule can help you or someone you know make the most informed decisions about Medicare coverage.

What Is the California Birthday Rule?

The California Birthday Rule allows Medicare beneficiaries who are already enrolled in a Medicare Supplement plan to switch to a different Medigap plan during a specific time period each year without answering health questions or undergoing medical underwriting. Medical underwriting usually requires insurance companies to review your health history before approving a plan. If you have certain health conditions, you might be denied coverage or charged higher premiums. The birthday rule removes that barrier and gives seniors more flexibility.

Who Qualifies for the Birthday Rule?

To use the California Birthday Rule:

- You must live in California

- You must already have a Medicare Supplement plan

- You can only use the rule during the 60 days following your birthday each year

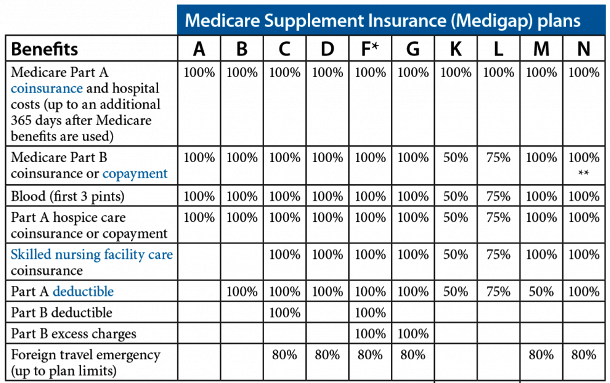

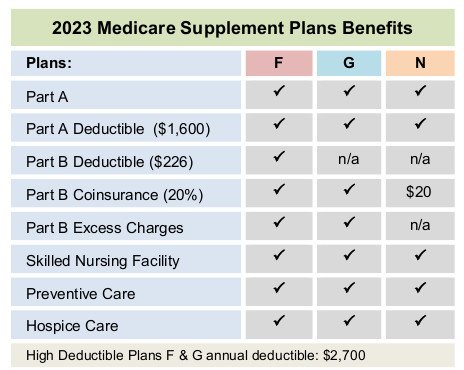

During this window you can switch to a different Medigap plan with “equal or fewer” benefits. For example, someone could switch from Plan G to Plan G or from Plan G to Plan N. You cannot use this rule to switch from a plan with fewer benefits, such as Plan N, to a plan with greater benefits, such as Plan G.

Why This Rule Matters

The birthday rule can be very helpful for seniors who want to reduce their monthly premiums, adjust coverage to better match their current health needs, or gain more predictable out-of-pocket costs. Without this rule, switching plans outside of your initial Medigap enrollment period may require medical underwriting, which can limit your options or increase costs. Even if you are satisfied with your current plan, knowing about the birthday rule ensures that you or someone you know is aware of all available options.

By reviewing available plans, I can often save clients hundreds and sometimes even thousands of dollars on their premiums each year.

How to Use the California Birthday Rule

- Mark your calendar because the rule applies during the 60 days following your birthday

- Review available Medigap plans to compare premiums and coverage

- Contact your insurance agent or insurance company to let them know you want to use the birthday rule to switch plans

- Complete the application because no health questions will be asked

- Confirm your coverage to make sure your new plan starts as expected

Planning ahead helps ensure you do not miss this opportunity because the window is limited.

Share This Information With Friends and Family

Many California seniors are unaware of the California Birthday Rule. Sharing this information with friends, family, or neighbors can help them avoid being denied coverage due to health conditions, reduce their premiums, or get a plan that better suits their needs. Providing this information is a valuable way to help others understand their Medicare options.

Need Help Understanding Your Options

Medicare rules can be confusing and every situation is a little different. If you or someone you know has a Medicare Supplement plan and wants to understand how the California Birthday Rule can help, I am always happy to answer questions and review options. Please feel free to share this article with friends or family who might benefit. Helping people understand their Medicare coverage is one of the most valuable things I can do for my clients.

Have Questions About Your Medicare Supplement Plan?

I’m here to help you understand your options and make the most of the California Birthday Rule. By reviewing available plans, I can often save clients hundreds and sometimes even thousands of dollars on their premiums each year.

If you found this article helpful, please feel free to share it with friends or family members who may have questions about their Medicare coverage.

Thank you!

Ron Lewis

CA agent #0B33674

NV agent #3822123

Ron@RonLewisInsurance.com

866.718.1600 (Toll-free)

760.525.5769 (Cell)

www.MedigapShopper.com

Congress passed this legislation to ensure that doctors would be paid adequately for providing Medicare services and to provide an incentive for doctors to continue accepting Medicare patients. Previous legislation had budgeted for doctors to have rate decreases over the years and there was concern that many doctors would stop accepting Medicare patients.

Congress passed this legislation to ensure that doctors would be paid adequately for providing Medicare services and to provide an incentive for doctors to continue accepting Medicare patients. Previous legislation had budgeted for doctors to have rate decreases over the years and there was concern that many doctors would stop accepting Medicare patients.