One of the most rewarding parts of my job is helping my clients save money on their Medicare Supplement (Medigap) insurance premiums. Most of the time, I can usually save individual clients at least $30 to $50 per month ($360 to $600 per year) on their premiums. Occasionally, I have saved them as much as $1,000 to $1,200 per year on their premiums!

I don’t mean to come across as bragging, because I’m not. However, I am very happy and excited because this past week I was able to save one of my clients (a husband and wife on a fixed income) over $5,300 per year on their Medicare Supplement premiums! I was able to do this just by simply switching them to the same exact plan that they had, but with a different carrier!

They had Plan G with another company for quite a few years, and they were very happy with the company and their coverage. Their insurance rates were very low when they originally took out their plans, and the company always paid their claims promptly and without a problem, just as most Medicare Supplement insurance companies do. However, over time, their rates crept up, slowly but steadily. Until this past week when they called me, they didn’t realize that they were literally paying thousands of dollars more for their insurance than they should be!

Most people shop around every year or two and compare rates on their auto and homeowner’s insurance. Medicare Supplements are no different. If you have a Medicare Supplement plan, it is critically important that you shop around every year and compare rates between various companies because insurance rates vary significantly from one carrier to the next for the same identical plan and coverage. For example…

For a 72 year old female living in the 92056 zip code, the current Plan F rates range from $164.06 per month to $245.50 per month! That is a difference of $81.44 per month or $977.28 per year more for the same exact insurance coverage!

Attained Age

In California, Medicare Supplement insurance premiums are based on attained age. This means that as you get older, your rates usually continue to go up every year. Many companies start off at the “younger” ages (65 to 70) with very competitive rates, but over time, the rates continue to go up. Every company is different, and some companies raise their rates a lot more than others.

If you become complacent and don’t shop around every year to compare rates, you are probably paying hundreds or even thousands of dollars more per year on your insurance premiums than you should be!

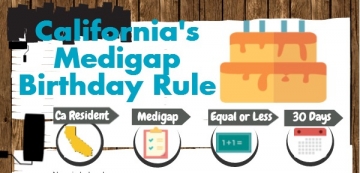

California Birthday Rule

In California, there is a law called the California Birthday Rule. This law allows anyone with a Medicare Supplement to switch to another insurance carrier every year within 30 days of their birthday (before or after), REGARDLESS OF THEIR HEALTH and without medical underwriting, if another insurance carrier is offering the same plan, such as Plan F, at a lower rate. During the annual 30-day open enrollment period, you are also guaranteed the right to switch to a “lesser” plan, such as from Plan F to Plan G, etc.

If you have a Medicare Supplement plan, you are guaranteed the right to shop around every year within 30 days of your birthday to save money on your insurance premiums. During this period, you cannot be turned down for coverage, regardless of your health.

You Can Apply for Medicare Supplement Plans All Year Long

Unlike Medicare Advantage plans that have an Annual Enrollment Period (AEP) from October 15th to December 7th every year for a January 1st effective date, you can apply for Medicare Supplement plans all year long. The only difference is that if you apply using the California Birthday Rule within 30 days of your birthday, you do not have to answer any of the health questions on the application, and you cannot be turned down for coverage due to health conditions.

If you apply for a Medicare Supplement plan any time of the year other than during your annual 30-day open enrollment period, you will have to answer the health questions on the application, and if you have certain health conditions, you could be turned down for coverage. If you are in relatively good health, you should not have any problem qualifying for a Medicare Supplement plan.

Guaranteed Issue Situations In California

In California, there are certain circumstances when you would qualify for a Medicare Supplement due to a guaranteed issue situation.

If you can answer YES to any of the following questions, you may be eligible for guaranteed issue:

- Has your employer-sponsored retiree plan that is supplementing Medicare involuntarily terminated?

- Has your employer-sponsored retiree plan stopped providing Medicare supplement benefits or the Medicare Part B 20% coinsurance for services?

- Have you lost eligibility for an employer-sponsored retiree plan due to divorce or death of a spouse or family member?

- Has your Medicare Advantage plan increased your premium or co-payments by 15% or more, reduced your benefits, or terminated its relationship with your medical provider who was treating you?

- Have you moved out of the area of your MA plan or Program for All-Inclusive Care for the Elderly (PACE) organization?

- Has your MA plan, Medicare SELECT Plan, PACE provider or any other health plan under contract with Medicare: (a) committed fraud; (b) ended or lost its contract with Medicare; (c) misrepresented the plan you bought, or (d) failed to meet its contractual obligations to Medicare beneficiaries, as determined by the federal government?

- Did you join a MA plan or PACE organization when you first became eligible for Medicare at age 65, and you want to switch to a Medicare Supplement policy during your first 12 months in the MA plan or PACE organization?

- Have you switched from a Medicare Supplement policy to a MA plan, PACE organization, Medicare SELECT plan, or any other health care organization contracting with Medicare, for the first time since becoming eligible for Medicare within the past 12 months?

- Has your MA plan left your area, and if so, did your MA plan benefits end within the past 123 days?

NOTE: Many people with Medicare Advantage plans who have serious health issues can still qualify for a guaranteed issue Medicare Supplement plan. See item #4 above.

What Insurance Carriers Do I Work With?

As a licensed independent insurance agent, I work with ALL the major insurance carriers in California. Most importantly, I WORK FOR YOU, not a particular insurance company! I’m also licensed in Arizona, Colorado, Nevada, and Washington state. Here are some, but not all, of the Medicare Supplement insurance carriers that I work with:

- Aetna

- Anthem Blue Cross

- Blue Shield of California

- Cigna

- Health Net

- Humana

- Individual Assurance Company (IAC)

- Mutual of Omaha

- Oxford

- Stonebridge

- Transamerica

- UnitedHealthcare (AARP)

- United of Omaha

Let Me Do the Shopping For You!

While it is unusual for me to be able to save most of my clients over $5,300 per year on their annual insurance premiums like I did this past week, it is not unusual for me to give someone a free, no obligation quote and save them anywhere from $300 to $500 per year on their Medicare Supplement premiums. That happens quite frequently.

As an independent insurance agent, I have access to insurance quote engines and other information that is not available to the public. You should take advantage of my knowledge and experience and let me do the shopping for you to save you money on your insurance premiums.

If you have a Medicare Supplement plan, please contact me for a free, no obligation quote. More than likely, I will save you hundreds of dollars on your Medicare Supplement insurance premiums.

If you have a Medicare Supplement plan, please contact me for a free, no obligation quote. More than likely, I will save you hundreds of dollars on your Medicare Supplement insurance premiums.

As one of my clients, I will contact you every year, about a month before your birthday, and I will let you know what the best rates are at that time. You always have the option to either keep your current plan, or you can take advantage of the California Birthday Rule and change carriers if another company is offering better rates.

Either way, I strive to build trust and relationships with my clients. I will not do a magic act and disappear after you have your new policy, 😉 and you will always have the peace of mind knowing that you are not paying hundreds or even thousands of dollars more than you should be for your Medicare Supplement insurance.

If you have any questions, or if you or anyone that you know would like a free Medicare Supplement quote, please contact me at (760) 652-6060 or toll-free at (866) 718-1600. You can also reach me by email at Ron@RonLewisInsurance.com. Your questions and feedback are always welcome!