Some Medicare beneficiaries are receiving new Medicare card numbers as part of ongoing fraud protection efforts

Recently, some Medicare beneficiaries have heard that new Medicare card numbers are being issued in 2026. Many people are wondering whether this affects them. Here is what you should know.

Are Medicare Card Numbers Changing This Year

Yes, but only for a small number of people. The Centers for Medicare & Medicaid Services is mailing new Medicare card numbers to certain beneficiaries as part of a security update related to fraud prevention. If you are affected, your new card will arrive automatically by mail. You do not need to request one.

NOTE:Most Medicare beneficiaries will not receive a new number.

Why Some Medicare Numbers Are Being Replaced

From time to time, the Centers for Medicare and Medicaid Services updates Medicare identification numbers for certain beneficiaries as part of ongoing efforts to protect personal information and reduce fraud. If your number is affected, Medicare automatically sends a replacement card by mail and no action is required from you.

What Should You Do If You Receive a New Medicare Card

If you receive a new Medicare card in the mail, you should do the following:

Start using the new number immediately

Safely destroy your old card

Share your new number with your doctors if needed

Let your insurance agent know so your records stay updated

There is no cost for a replacement Medicare card. If your Medicare card is lost or damaged, you can request a replacement card at any time through your secure account at Medicare.gov or by calling (800) MEDICARE. Replacement cards are mailed directly from Medicare and there is never a fee for this service.

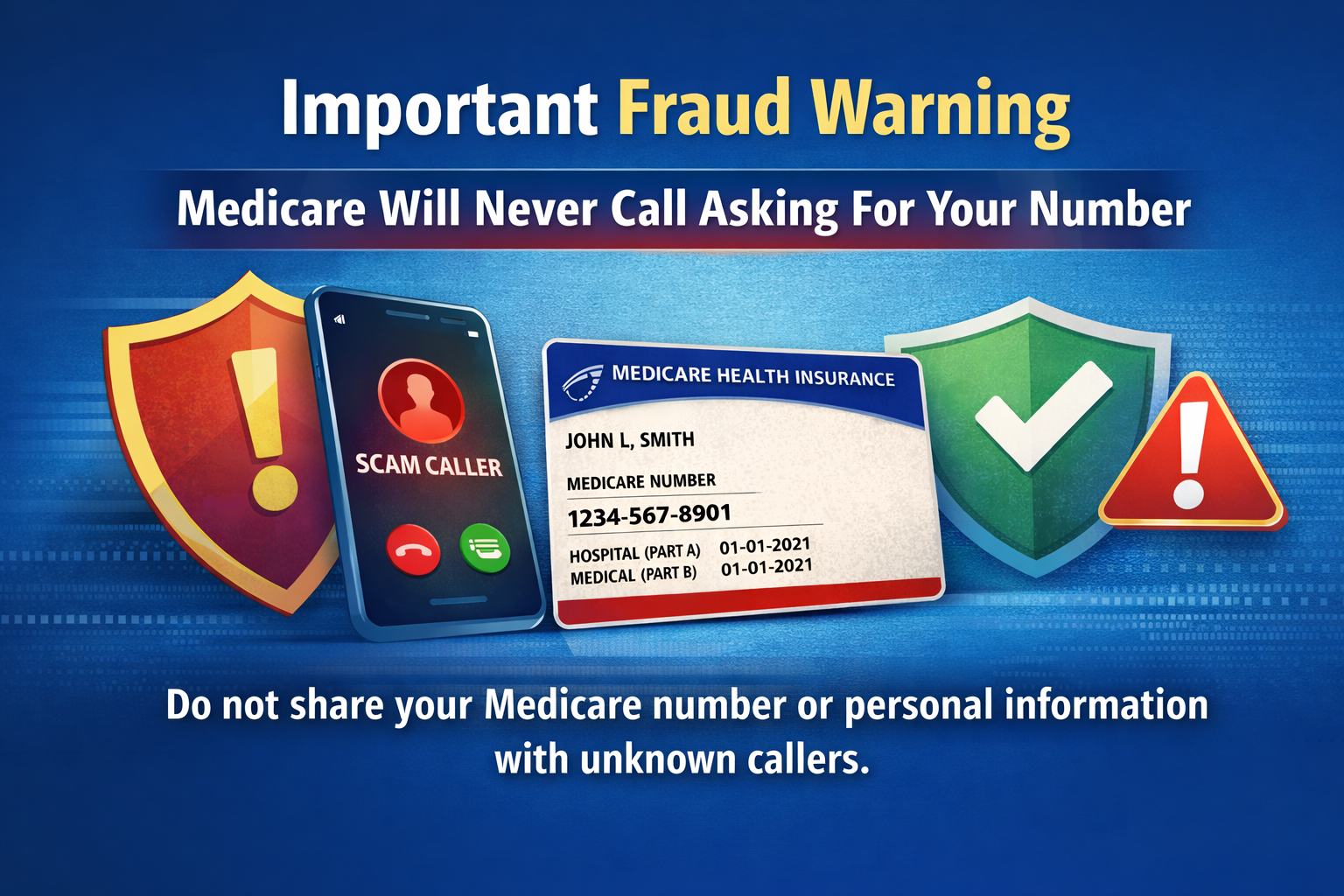

Important Fraud Warning

Medicare will never call unexpectedly asking for your Medicare number

Unfortunately, scammers often take advantage of situations like this.

Please remember that Medicare will never do any of the following:

Call you unexpectedly to ask for your Medicare number

Charge you for a replacement card

Ask for banking information to send a new card

Threaten that your coverage will be cancelled unless you respond immediately

Send plastic or chip Medicare cards

IMPORTANT:If someone contacts you and asks for personal information related to your Medicare card, it is very likely a scam.

How To Recognize An Official Medicare Mailing

An official Medicare mailing does the following:

Arrives by postal mail

Does not request payment

Does not ask for banking information

Includes your name exactly as shown on your Medicare card

Does not require immediate action to keep your coverage active

If something feels urgent or requests personal information, it is best to verify it before responding.

What Should You Do If You Receive a Suspicious Call

If you receive a suspicious call about Medicare, the safest step is to contact Medicare directly at (800) MEDICARE to confirm whether the request is legitimate. You are also welcome to contact me if you would like help reviewing anything you receive.

Where To Learn More About Medicare Fraud Prevention

If you would like additional information about how to protect yourself from Medicare fraud, these official resources can help:

These trusted sources explain warning signs and what steps to take if something does not seem right.

My Recommendation to Clients

If anyone contacts you about your Medicare card and you are unsure what to do, it is always best to verify the request before responding. Protecting your Medicare information helps prevent fraud and keeps your coverage secure.

If you ever receive a Medicare related notice and are unsure whether it applies to your coverage, I am always happy to help review it with you.

About the Author

I’m an independent Medicare Supplement insurance specialist working with most of the major insurance carriers throughout California, Nevada, and several other states. I help people turning 65 coordinate their Medicare enrollment so their Medicare Supplement and prescription drug coverage begin at the same time as Medicare.

I also work with many people who already have Medicare Supplement plans and would like to review their options. In California, the Medicare Supplement Birthday Rule allows policyholders to change their plans each year without medical underwriting, and I regularly help clients lower their premiums while keeping the same identical plan and coverage. Many of my clients have saved hundreds, and sometimes thousands, of dollars.

There is no charge for my services because I am compensated by the insurance carriers, not my clients. My goal is to help you find competitive premiums and provide dependable personal service year after year.

If you are turning 65 soon, or if you already have a Medicare Supplement plan and would like to review your options, I am happy to help.

You can also click here to read what my clients have to say about working with me.

Serving Medicare clients throughout California, Nevada, and several other states.

CA Insurance License: #0B33674 NV Insurance License: #3822123 AZ Insurance License: #681166

This website is operated by a licensed insurance agent and is intended for educational purposes only. I am not affiliated with or endorsed by Medicare or any government agency.

This blog is a step by step guide explaining when to enroll, whether you can sign up by phone or online, and how to coordinate Medicare with a Medicare Supplement plan.

The Medicare Initial Enrollment Period lasts 7 months. Applying during the 3 months before your birthday month helps ensure your Medicare and Medicare Supplement coverage start on time.

Turning 65 is an important milestone and for most Americans it means becoming eligible for Medicare. Many people turning 65 are surprised to learn that signing up for Medicare and choosing their coverage options involves several coordinated steps. Many people are unsure how to sign up, when to enroll, and which method is easiest. This blog explains the different ways to enroll in Medicare and which options work best depending on your situation.

Are You Automatically Enrolled in Medicare?

Some people are enrolled in Medicare automatically. You will usually be automatically enrolled in Original Medicare (Part A – Hospital insurance) and (Part B – Medical insurance) if you are already receiving Social Security retirement benefits at least four months before your 65th birthday.

If you are automatically enrolled:

Your Medicare card usually arrives about three months before your 65th birthday.

Coverage usually starts the first day of your birthday month (or the first day of the previous month if your birthday is on the 1st of the month).

No Medicare application is required unless you want to delay Part B.

If you are not receiving Social Security benefits yet, you will need to apply for Medicare yourself.

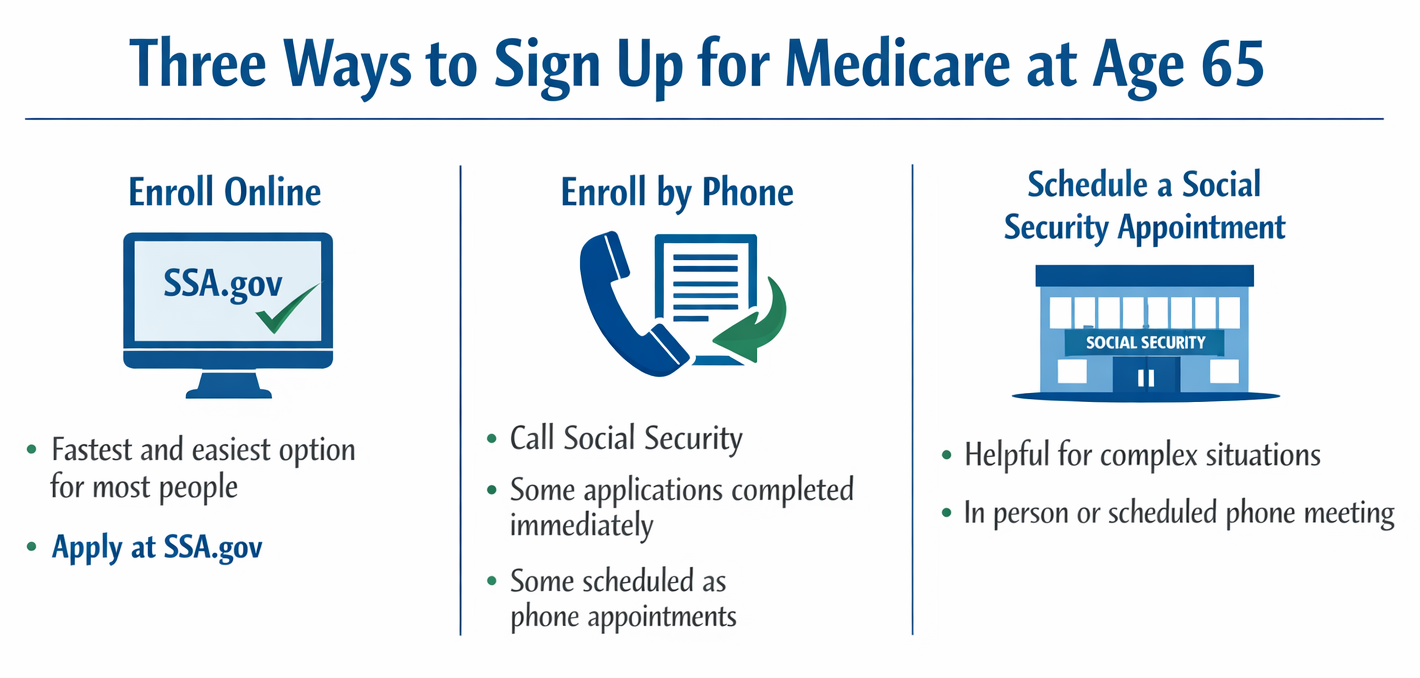

The Three Main Ways to Sign Up for Medicare

Most people turning 65 can sign up for Medicare online through Social Security by phone or by scheduling a Social Security appointment. Choosing the right enrollment method can help ensure your coverage starts on time.

If you need to enroll yourself, there are three main options:

1. Enrolling Online Through the Social Security Website

For most people turning 65, enrolling online through the Social Security website is the fastest and easiest method. Please click here to enroll online.

NOTE:I know it seems counter-intuitive, but you go to the Social Security website, not the Medicare website, to sign up for Medicare.

Advantages of online enrollment include the following:

Available twenty-four hours a day.

No waiting on hold.

Typically processed quickly.

Often completed in about fifteen minutes.

Best for the following situations:

People retiring at 65.

Individuals not covered by employer insurance.

Anyone comfortable using a computer.

For most applicants, this is the best and simplest way to enroll.

2. Enrolling by Phone With Social Security

Many people prefer speaking with a representative. You can still enroll in Medicare by calling Social Security at (800) 772-1213.

Sometimes enrollment can be completed during the call. In other cases, Social Security schedules a follow up phone appointment with a specialist who completes the application with you.

Advantages of phone enrollment include the following:

Helpful if you have questions.

Useful for coordinating employer coverage with Medicare.

Comfortable option for people who prefer personal assistance.

Best for the following situations:

Applicants delaying Part B because they are still working.

Individuals enrolling during a Special Enrollment Period.

People who want guidance through the process.

3. Enrolling Through a Local Social Security Office

Some applicants prefer in person assistance. You can schedule an appointment with your local Social Security office to apply for Medicare. To set up an appointment, call Social Security at (800) 772-1213. Most offices now require appointments instead of walk in visits.

Advantages of in person enrollment include the following:

Face to face support.

Helpful for complicated situations.

Useful if documentation is required.

Best for the following situations:

Applicants with unique eligibility situations.

Individuals who prefer meeting with someone directly.

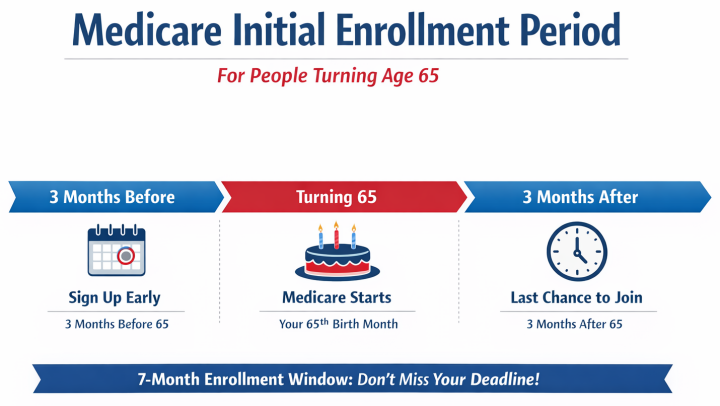

When Should You Apply for Medicare?

Your Initial Enrollment Period (IEP) lasts seven months:

Three months before your 65th birthday month.

Your birthday month.

Three months after your birthday month.

Applying during the three months before your birthday month helps ensure your coverage starts on time.

What If You Are Still Working at Age 65?

If you or your spouse are still working and covered by employer health insurance, you may be able to delay Part B without penalty. This depends on the size of the employer and the type of coverage you have. Many people in this situation enroll in Part A (Hospital insurance) only and delay Part B (Medical insurance) until retirement. Before delaying Part B, it is important to confirm that your employer coverage qualifies. Please click here for more details.

NOTE:Part A is usually free, but the monthly premium for Part B is currently $202.90 for most people (in 2026), unless you are in a higher income bracket. If you are still working, you can usually defer paying the Part B premium until you leave your employer health plan.

Common Mistakes People Make When Signing Up for Medicare

Here are some common mistakes people make when signing up for Medicare:

Waiting too long to apply and risking delayed coverage.

Assuming enrollment happens automatically when it does not.

Delaying Part B without confirming employer coverage rules.

Missing the six month Medicare Supplement Open Enrollment window after Part B begins.

Avoiding these mistakes can save money and prevent future coverage problems.

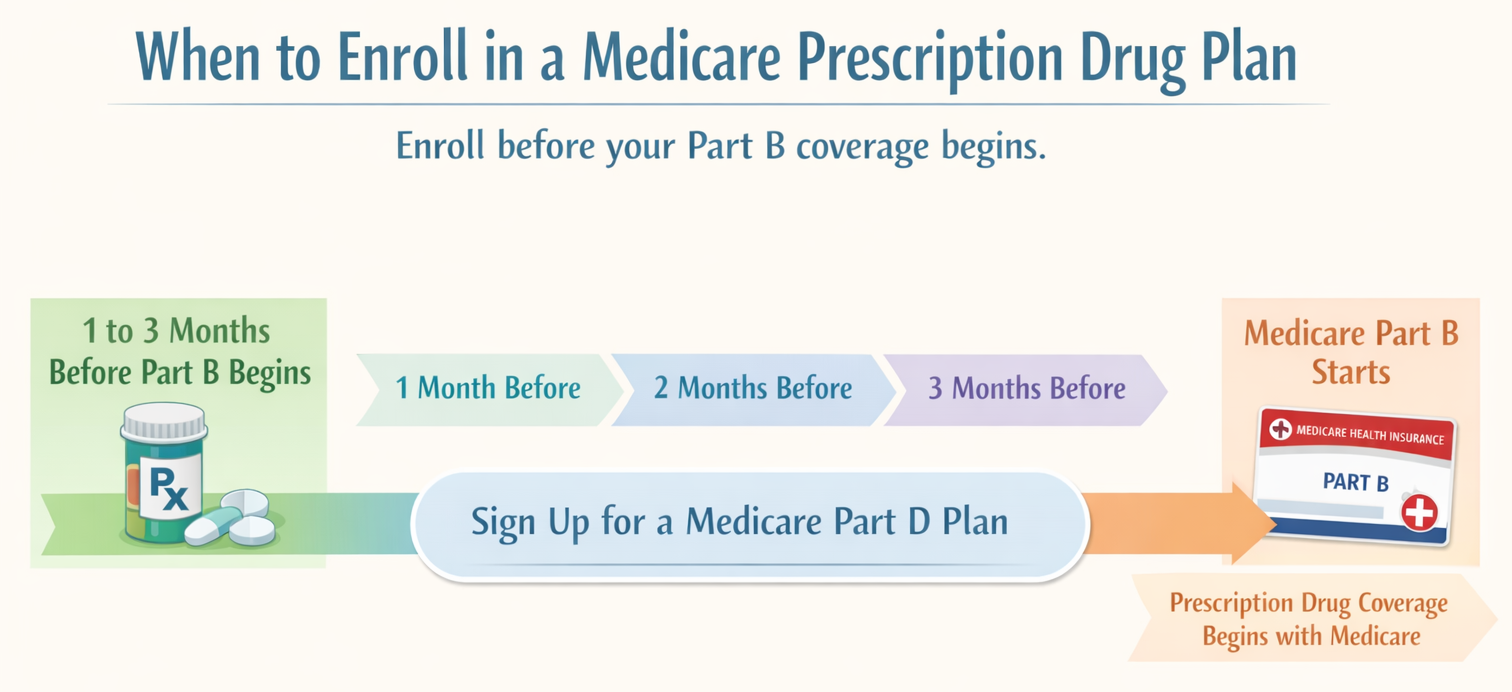

Do You Need to Enroll in a Medicare Part D Prescription Drug Plan?

When you first become eligible for Medicare, it is important to consider whether you should enroll in a Medicare Part D prescription drug plan. If you do not enroll in a Part D plan when you are first eligible and you do not have other creditable prescription drug coverage, you may have to pay a lifetime late enrollment penalty if you enroll later. Creditable prescription drug coverage usually includes employer or union coverage that is expected to pay at least as much as standard Medicare prescription drug coverage. It is important to confirm whether your existing coverage is considered creditable before deciding to delay Part D enrollment.

IMPORTANT: Even if you do not currently take prescriptions, enrolling in a low cost Part D plan when you first become eligible can help you avoid future penalties. In California, some Medicare Part D plans are available with a $0 monthly premium, which makes enrolling early an easy way for many people to avoid future penalties while keeping costs low.

It is also important to know that Medicare Supplement plans do not include prescription drug coverage. A separate Part D plan is needed if you want prescription coverage. Most people choose to enroll in a Part D plan when their Medicare Part B begins so their prescription coverage starts at the same time as their medical coverage.

The timeline below shows when to enroll in a Medicare Part D plan so your prescription coverage begins at the same time as Medicare.

Enrolling in a Medicare Part D prescription drug plan when you first become eligible helps ensure prescription coverage begins on time and helps avoid lifetime late enrollment penalties if you enroll later.

How to Sign Up for a Medicare Prescription Drug Plan

Here are the most common ways to sign up for a Medicare Prescription Drug Plan:

Option 1: Enroll online (recommended) Visit Medicare.gov and use the Plan Finder tool to compare all available Part D plans in your area. This allows you to review premiums, pharmacy networks, and estimated drug costs side-by-side so you can choose the plan that best fits your needs.

Click here to watch a short video I made that explains step-by-step how to sign up for a prescription drug plan.

Because many insurance agents are not appointed with every Part D carrier, and many agents no longer offer Part D enrollment assistance due to increasingly complex CMS compliance requirements, Medicare.gov is often the best place to make sure you’re seeing every available option.

Click here to read another blog I wrote explaining why you may be better off shopping for your own prescription drug plan instead of using an insurance agent.

Option 2: Enroll by phone Call 1-800-MEDICARE (1-800-633-4227) and a Medicare representative can help you review your options and complete enrollment.

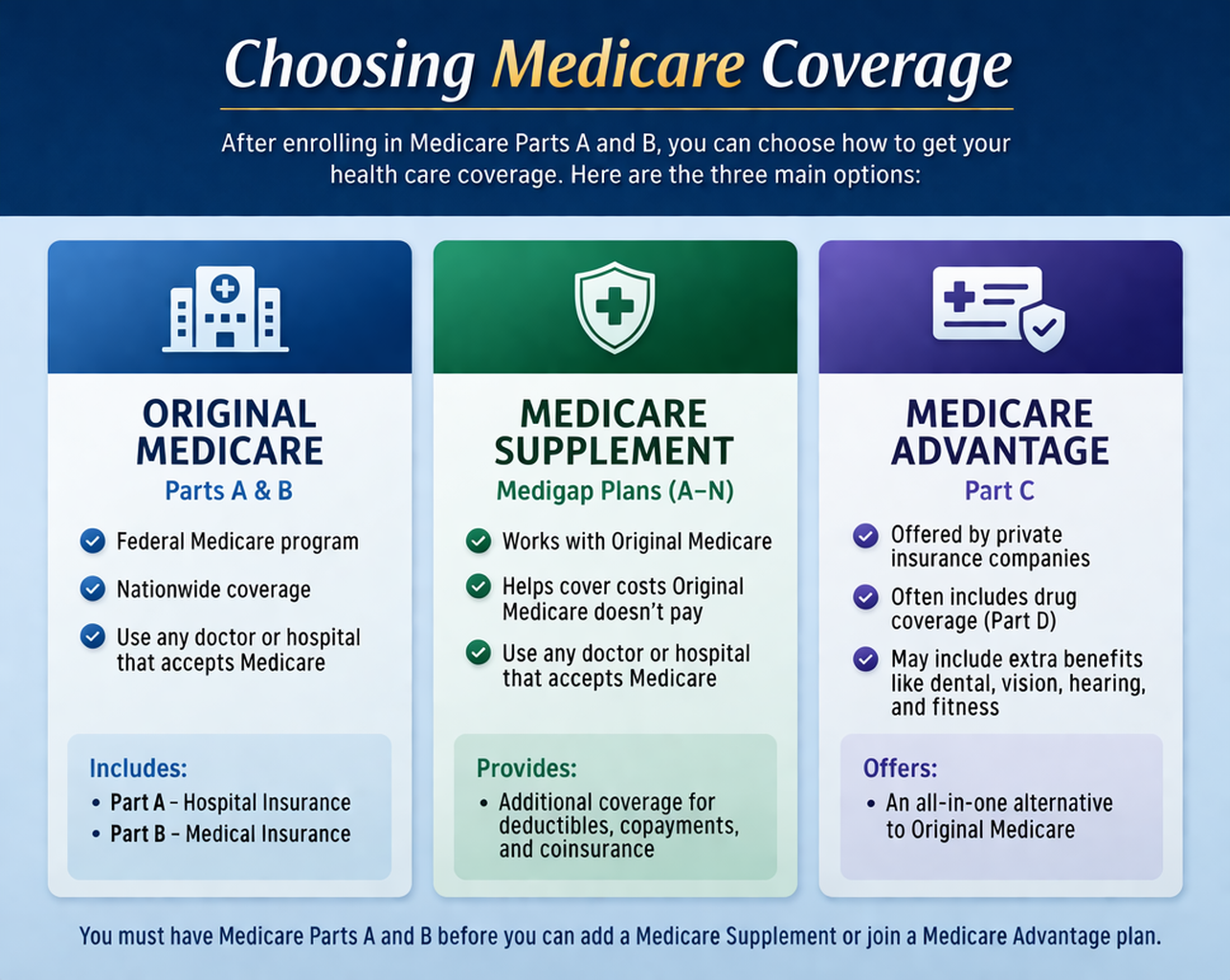

What Happens After You Enroll in Original Medicare?

Once you are enrolled in Original Medicare (Part A and Part B), it’s important to understand that Original Medicare typically covers about 80% of approved medical expenses, and there is no limit on your out-of-pocket costs. Because of this, most people choose to add additional coverage.

Your main options include:

A Medicare Supplement plan (also called Medigap)

A Medicare Advantage plan

A Part D prescription drug plan

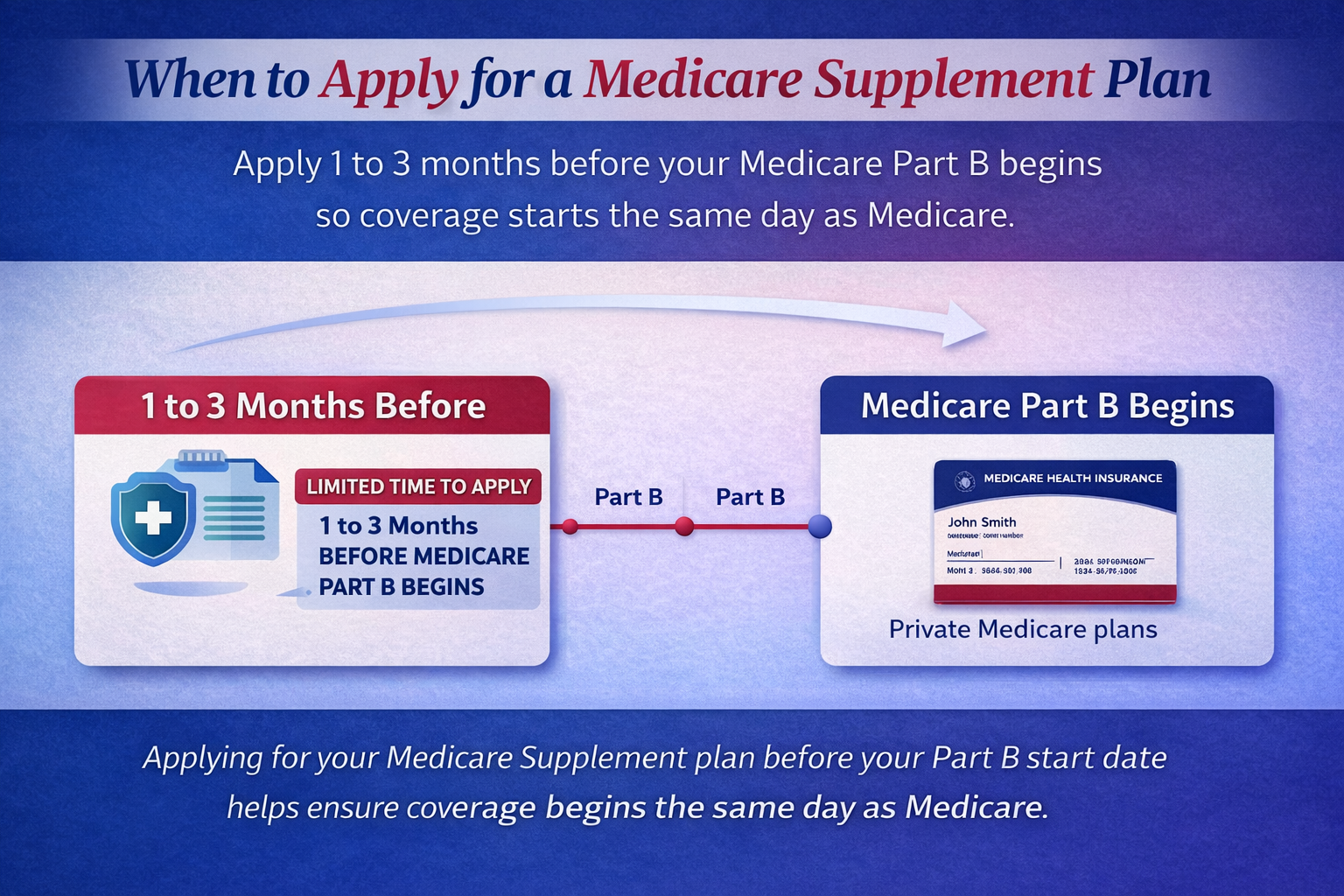

If you choose a Medicare Supplement plan, which many people prefer because it helps limit unexpected out-of-pocket costs, the best time to apply is before your Medicare Part B effective date so your coverage can begin the same day your Medicare coverage starts. Many people submit their Medicare Supplement application one to three months before their Part B start date to help avoid any gap in coverage.

Your six-month Medicare Supplement Open Enrollment Period begins when your Part B coverage starts. During this six-month window, you cannot be turned down or denied coverage due to health conditions. However, applying before your Part B effective date helps ensure your Medicare Supplement coverage starts on time.

Some people choose a Medicare Advantage plan as an alternative way to receive their Medicare benefits. However, there are important differences between Medicare Advantage plans and Medicare Supplement plans.

Click here to read my article explaining why many people carefully compare these options before choosing a Medicare Advantage plan.

A Simple Checklist for Turning 65

Find out whether you will be automatically enrolled.

Decide whether you should delay Part B because of employer coverage.

Choose whether to apply online, by phone, or through a Social Security appointment.

Apply during the three months before your birthday month when possible.

Review Medicare Supplement options once your Part B start date is confirmed.

Understanding the Difference Between Enrolling in Medicare and Enrolling in a Medicare Supplement Plan

Signing up for Medicare and signing up for a Medicare Supplement plan are totally different. Enrolling in Medicare is done through Social Security and determines when your Part A and Part B coverage begin. Enrolling in a Medicare Supplement plan is done through a private insurance company using an insurance agent and helps cover most of the out of pocket costs that Original Medicare does not pay.

Many people assume these steps happen automatically together, but they do not. Coordinating the timing of your Medicare Supplement application with your Part B start date helps ensure your coverage begins the same day your Medicare coverage becomes active.

Medicare Supplements and Medicare Advantage Plans Are Totally Different

After enrolling in Original Medicare, most people choose either a Medicare Supplement or a Medicare Advantage plan. Understanding the difference between these options is an important step when planning your Medicare coverage.

After enrolling in Medicare Part A and Part B, most people choose either a Medicare Supplement plan or a Medicare Advantage plan. These are two different types of coverage and they work in very different ways. A Medicare Supplement works alongside Original Medicare and helps pay most out of pocket costs such as deductibles and coinsurance. A Medicare Advantage plan replaces Original Medicare coverage with a private plan that includes provider networks and different cost structures. Most Medicare Advantage plans are HMOs and your choices are limited.

Understanding the difference between these options is an important step when planning your Medicare coverage.

A Medicare Supplement Insurance Specialist Helps Coordinate Your Start Date

Applying for a Medicare Supplement plan one to three months before your Medicare Part B start date helps ensure there are no gaps in coverage when Medicare begins.

One of the most helpful things a Medicare Supplement insurance specialist can do is coordinate the timing between your Medicare Part B effective date and your Medicare Supplement application. Submitting your Medicare Supplement application before your Part B start date helps ensure your coverage begins the same day your Medicare coverage becomes active. This helps prevent gaps in coverage and allows you to move into Medicare with confidence.

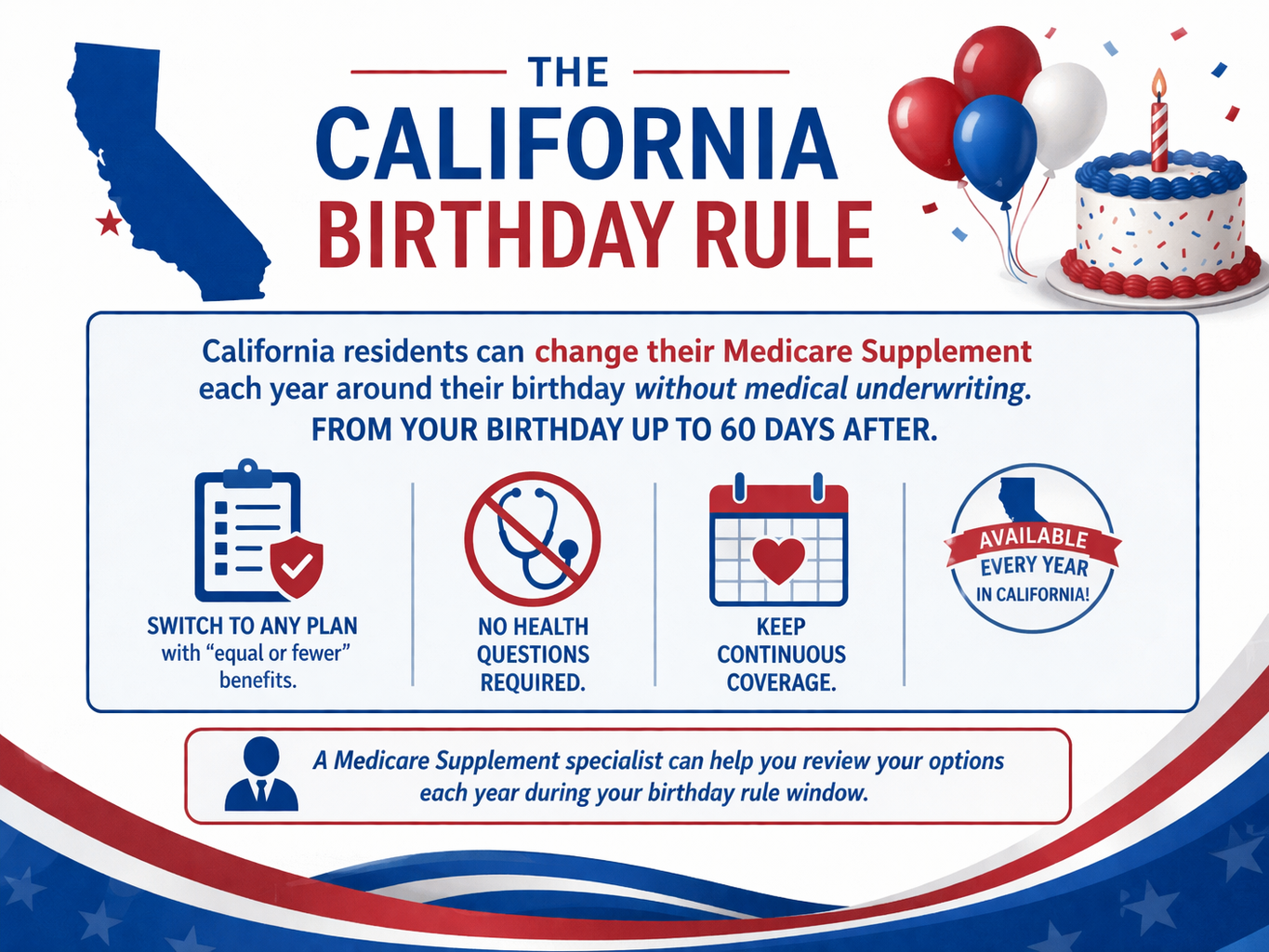

California Residents Have an Additional Medicare Supplement Advantage

California residents can change their Medicare Supplement each year from their birthday up to 60 days after. No health questions required when switching to a plan with “equal or fewer” benefits.

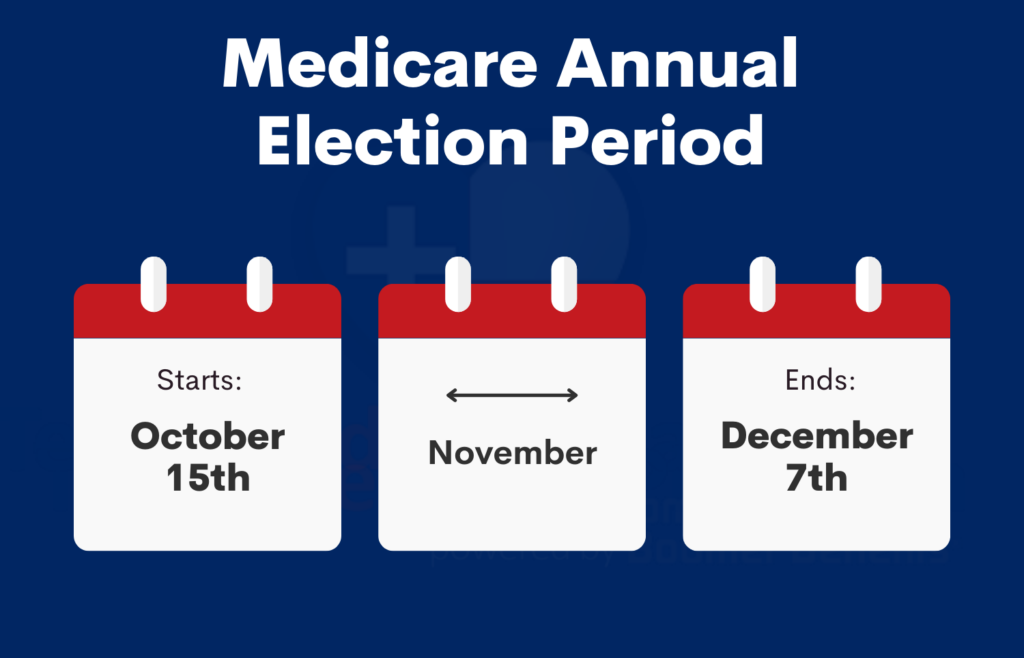

With a Medicare Advantage plan, you can generally only change your coverage during the Annual Election Period (AEP), which runs from October 15th through December 7th each year, unless you qualify for a Special Enrollment Period. Coverage selected during this time begins on January 1st of the following year.

With a Medicare Supplement, you can apply to change coverage at any time during the year. However, in most cases, you will need to answer health questions and go through medical underwriting.

California residents have an added advantage under the California Birthday Rule. This law provides a 60-day window beginning on your birthday each year. During this time, you can switch to another Medicare Supplement plan with the “same or fewer” benefits without medical underwriting.

For example, if you have Plan G, you can switch to Plan G with any other insurance carrier, regardless of your health. In contrast, most states do not offer a birthday rule, which means individuals with health conditions may be unable to change plans or carriers without underwriting. If you are in California, it is a good idea to review your Medicare Supplement options around your birthday each year. I do this for my clients to help them take advantage of potential savings.

If you would like help reviewing your Medicare Supplement options or seeing if you may qualify for savings under the California Birthday Rule, I offer no cost consultations and would be happy to help you explore your options.

Final Thoughts

Signing up for Medicare does not have to be confusing. Understanding your enrollment options ahead of time helps ensure your coverage starts on time and helps you avoid unnecessary penalties or gaps in coverage.

If you are turning 65 soon and would like help coordinating your Medicare enrollment with a Medicare Supplement plan so your coverage begins on time, speaking with a licensed Medicare specialist can make the process much easier and more confident.

If you would like personalized help reviewing your Medicare Supplement options or timing your enrollment correctly, my contact information is below.

About the Author

I’m an independent Medicare Supplement insurance specialist working with most of the major insurance carriers throughout California, Nevada, and several other states. I help people turning 65 coordinate their Medicare enrollment so their Medicare Supplement and prescription drug coverage begin at the same time as Medicare.

I also work with many people who already have Medicare Supplement plans and would like to review their options. In California, the Medicare Supplement Birthday Rule allows policyholders to change their plans each year without medical underwriting, and I regularly help clients lower their premiums while keeping the same identical plan and coverage. Many of my clients have saved hundreds, and sometimes thousands, of dollars.

There is no charge for my services because I am compensated by the insurance carriers, not my clients. My goal is to help you find competitive premiums and provide dependable personal service year after year.

If you are turning 65 soon, or if you already have a Medicare Supplement plan and would like to review your options, I am happy to help.

You can also click here to read what my clients have to say about working with me.

Serving Medicare clients throughout California, Nevada, and several other states.

Ron Lewis Ron@RonLewisInsurance.com www.MedigapShopper.com (760) 525-5769 (866) 718-1600

Choosing a Medicare Prescription Drug Plan (PDP), which is also known as Part D, can feel overwhelming. With dozens of plans available, each with different premiums, deductibles, copays, and pharmacy networks, it’s easy to make a costly mistake.

As a Medicare Supplement (Medigap) insurance agent, I often get questions from clients who also want help selecting a Part D plan. While I’d love to help, I recently learned that helping someone choose or enroll in a Part D plan without proper certification could put my insurance license at risk. However, there’s a better option that is free, unbiased, and comprehensive through the Health Insurance Counseling and Advocacy Program (HICAP).

Many Insurance Agents Have Stopped Selling Prescription Drug Plans

If you’ve noticed that fewer independent agents are offering Medicare Prescription Drug (Part D) plans, you’re not imagining things. Over the past couple of years, the Centers for Medicare & Medicaid Services (CMS) has introduced an increasing number of onerous regulations that have made it extremely difficult for many agents to continue offering these plans, especially independent agents who value personal service and client relationships.

For example, CMS recently began requiring insurance agents to record every marketing, sales, and enrollment call related to Medicare Prescription Drug Plans (Part D). This means any discussion involving benefits, costs, or plan comparisons must be recorded, both inbound and outbound, and those recordings must be securely stored for 10 years. Agents don’t like this and many Medicare beneficiaries don’t want their conversations recorded.

While these rules were intended to protect consumers from misleading marketing, the burden of compliance has become overwhelming for many professionals in the field. For more detailed information, please click here to check out my other blog called “Why Many Insurance Agents Have Stopped Selling Prescription Drug and Advantage Plans,” and click here to to check out another related blog called “Why You May Be Better Off Choosing Your Own Medicare Prescription Drug Plan (Part D).”

Why an Insurance Agent Might Not Be Enough

Many insurance agents are only certified to sell PDP’s from certain insurance carriers, which means:

They may not have access to every plan available in your area.

Their guidance could be influenced by commissions or appointments, even unintentionally.

You may not get a complete picture of your options, which can lead to higher costs or gaps in coverage.

That’s where HICAP comes in.

What is HICAP and How It Helps

The Health Insurance Counseling and Advocacy Program (HICAP) is a free, state-run program in California that provides free, confidential one-on-one counseling, education, and assistance to individuals and their families on Medicare, Long-Term Care insurance, other health insurance related issues, and planning ahead for Long-Term Care needs.

HICAP also provides legal assistance or legal referrals in dealing with Medicare or Long-Term Care insurance related issues. HICAP counselors are trained in Medi-Cal and Medicare and can help you understand the complex insurance options to find the best fit for you.

HICAP counselors:

Can show all available Part D plans in your area.

Provide completely unbiased guidance, with no sales pressure.

Help you compare costs, deductibles, co-pays, and pharmacy networks.

Walk you through the Medicare Plan Finder tool or help you understand your plan options.

What HICAP Services Are Available?

HICAP can help you with the following:

Have questions on prescription drug coverage, co-pays, or eligibility rules?

Wondering how to sign up for Medicare now that you are almost 65?

Confused about all the different parts to Medicare, do you need A, B, C, D?

Need help filing an appeal or challenging a denial?

Considering long-term care insurance?

Need a speaker for a community education event?

How a HICAP Session Works

Whether over the phone or in person, the process is simple:

Prepare your information: Have a list of all your prescriptions, your preferred pharmacy, and your zip code.

Enter your own prescriptions: You input your medication information into Medicare.gov.

Guided support: The HICAP counselor explains your options, interprets plan details, and answers questions.

Compare plans: They help you see which plan offers the best coverage for your needs.

Enrollment: You complete the enrollment yourself online or by calling the plan.

Who Can Get These Services?

Counseling is provided to the following individuals:

Persons 65 years of age or older and are eligible for Medicare

Persons younger than age 65 years of age with a disability and are eligible for Medicare

Persons soon to be eligible for Medicare

Why HICAP is the Best Choice

HICAP counselors provide a full picture of your options, which an insurance agent cannot always do. Their guidance is independent, comprehensive, and free. This ensures you make an informed decision about your prescription coverage without missing important details or paying more than necessary.

Check Out My Video — How to Sign Up for a PDP on the Medicare Website

This past year, I created a step-by-step YouTube video that shows you how to use the Medicare Plan Finder tool. Nothing has changed since last year. Instead of contacting a HICAP counselor, you should be able to watch the video and be able to select a PDP and enroll on your own. It’s really very easy! Please click here to watch the video. It’s only 14 minutes long.

Next Steps

If you’re ready to compare Medicare Prescription Drug Plans for 2026:

Click here to watch my Youtube video that explains how to to use the Medicare Plan Finder tool to select a PDP and enroll on your own.

Call HICAP at 1-800-434-0222 or click here to find a local office in California.

In other states besides California, you can get help at your local State Health Insurance Assistance Program (SHIP). Their phone number is 1-877-839-2675 or click here to find a local office outside of California.

And if you have questions about Medicare Supplement (Medigap) plans, I’m here to help guide you through your options.

Conclusion

Choosing a Part D plan doesn’t have to be stressful. By using HICAP’s free, unbiased services, you can get all the information you need to make the best decision for your health and budget, while staying in control of the process.

About the Author

As an independent Medicare Supplement insurance specialist, I work with most of the major insurance carriers throughout California, Nevada, Arizona, and several other states. I shop around for my clients every year during their 60-day annual open enrollment period under the California Birthday Rule to help them save money on their Medicare Supplement premiums. Many of my clients have saved hundreds, even thousands of dollars on the same exact plan and coverage! Please click here to see what my clients have to say about my services.

There is no charge for my services as I’m compensated by the insurance carriers, not my clients. My goal is to help you find the lowest premiums and provide the best personal service possible, year after year. Unlike many agents, I won’t do a magic act and disappear after you sign up! 🙂

If you enjoyed this blog and found it helpful, please leave your comments, questions, or feedback below and feel free to share this article with your friends!

Thank you!

Ron Lewis Ron@RonLewisInsurance.com www.MedigapShopper.com (760) 525-5769 – Cell (866) 718-1600 – Toll-free

Each year, many people in California decide to leave their Medicare Advantage (Part C) plan and return to Original Medicare (Part A and Part B) with a Medicare Supplement (Medigap) plan. Often, this happens when premiums, copays, or out-of-pocket costs increase, or when clients find their favorite doctors or hospitals are no longer in their plan’s network.

If you’ve ever wondered how to switch from Medicare Advantage to Medigap, it’s important to understand how the process works, and the potential challenges if you have existing health conditions.

You Can Switch Back to Original Medicare — But You’re Not Automatically Guaranteed Medigap Approval

You can drop your Medicare Advantage plan and go back to Original Medicare during certain times of the year, such as the Annual Election Period (AEP), which goes from October 15th through December 7th every year or during the Medicare Advantage Open Enrollment Period, which goes from January 1st through March 31st.

However, many people are surprised to learn that once they return to Original Medicare, they must apply separately for a Medicare Supplement plan, and approval is not guaranteed. In most cases, insurance companies can review your health history, which is called “medical underwriting,” and deny coverage if you have serious or chronic health conditions. That’s why timing and knowing the rules can make all the difference.

Medicare Guaranteed Issue Rights: The Hidden Opportunities

Here’s the good news… even if you have health problems, there are special Guaranteed Issue (GI) rights or situations that often let you enroll in a Medigap plan without health questions or underwriting.

These rights apply in specific situations and many beneficiaries don’t realize they qualify. Some are tied to Medicare Advantage plan changes, others to state-specific protections. In California, there are several lesser-known GI opportunities that can help people switch to Medigap coverage, even when they’ve been told “no” before.

I work with clients every year who thought they couldn’t qualify due to health issues and I’ve helped them get accepted for Medicare Supplement coverage using legitimate Guaranteed Issue options that most agents aren’t aware of or don’t mention to their clients.

Why Work with a Specialist Who Knows the California Rules

The Medicare rules in California are unique. Between the California Birthday Rule and other state-specific guaranteed issue protections, there are several ways to save money and secure coverage without medical underwriting.

As an independent Medicare Supplement insurance specialist, I work with all the major insurance carriers throughout California, Nevada, and several other states. My goal is simple. I want to help you find the best Medicare Supplement plan with the lowest premium and the most reliable coverage, year after year.

Let’s See What You Qualify For

If you’re considering leaving your Medicare Advantage plan or want to see if you qualify for a Guaranteed Issue Medicare Supplement, don’t wait until it’s too late.

There is no cost for my help. I’m paid by the insurance carriers, not my clients. I can review your situation, identify any Guaranteed Issue opportunities, and help you apply for the coverage that fits your needs and budget.

Contact me today to learn your options and see how much you could save on your Medicare Supplement plan.

About the Author

As an independent Medicare Supplement insurance specialist, I work with all the major insurance carriers throughout California, Nevada, and several other states. I shop around for my clients every year during their annual open enrollment period under the California Birthday Rule to help them save money on their Medicare Supplement premiums. Many of my clients have saved hundreds, even thousands of dollars for the same exact plan and coverage! Please click here to read what my clients have to say about my services.

There is no charge for my services as I’m compensated by the insurance carriers, not my clients. My goal is to help you find the lowest premiums and provide the best personal service possible, year after year. Unlike many agents, I won’t disappear after you sign up!

If you enjoyed this blog and found it helpful, please leave your comments, questions, or feedback below and feel free to share this article with your friends!

Thank you!

Ron Lewis Ron@RonLewisInsurance.com www.MedigapShopper.com (760) 525-5769 – Cell (866) 718-1600 – Toll-free

If you’ve ever tried to compare Medicare Prescription Drug Plans (PDPs), also known as Medicare Part D, you know how confusing it can be. There are dozens of options, and each plan has its own list of covered drugs (called a formulary), preferred pharmacies, and cost structure. What looks like a small difference in co-pays or premiums can easily add up to hundreds of dollars over the course of a year.

Why Most Agents No Longer Sell Prescription Drug Plans

You might assume that a licensed insurance agent can help you find the best plan, and in the past, many could. However, today’s system makes that much more difficult. Because of how Medicare’s certification and contracting rules work, most independent agents are not certified with every drug plan available in your area. They can only recommend or enroll you in a limited number of specific plans they are contracted with and certified to sell.

If another company offers a plan with lower co-pays or better coverage for your medications, your agent may not even be allowed to discuss it with you. Why? Because they don’t get paid for selling plans they’re not certified or contracted to represent. Even if they know a different plan would save you money, compliance rules and commission structures prevent them from showing it to you.

The Hidden Time and Cost Burden on Agents

Before an agent can help anyone with a PDP or a Medicare Advantage (MA) plan, they must complete extensive training and certification every year. This starts with the AHIP certification exam, which takes many agents 10–20 hours of study time to complete. The AHIP exam covers topics such as Medicare compliance, plan rules, CMS marketing guidelines, etc.

But that’s only the beginning. Agents must also spend time studying and taking individual certification exams for EVERY insurance company whose plans they want to sell. Each carrier’s certification process is different. Some require several hours of training, testing, and annual renewal. Altogether, a well-rounded agent could easily spend 50+ hours each year just keeping up with certifications before they can even begin helping clients.

Then there are the CMS compliance rules, which now require all sales calls related to PDPs and MA plans to be recorded and stored securely for 10 years! The added administrative burden and potential liability make it even less practical for agents to offer these plans, especially since commissions for prescription plans are typically under $100 per year per client. Many agents have simply decided that it’s not worth the time and effort.

How You Can Shop and Enroll in a Drug Plan On Your Own

Fortunately, Medicare makes it easy for you to shop around on your own and sign up for a prescription drug plan at www.Medicare.gov by using the exact same tool that agents use.

This past year, I put together a short video that explains how to shop for and sign up for a Medicare prescription drug plan using the Medicare Plan Finder tool. It’s actually very easy, and there aren’t any significant changes since last year. Please click here to watch the video.

The Medicare Plan Finder is available 24/7 and it is updated every fall with the latest plan information. It allows you to make an informed decision without pressure or bias, and without worrying whether your agent is certified to sell a particular plan.

Review Your Coverage Each Fall

Even if you’re happy with your current PDP, it’s important to review your coverage each year during the Annual Election Period (AEP), which goes from October 15th through December 7th each year. PDPs are annual contracts, and drug prices, plan premiums, and pharmacy networks can change every year. What’s good this year may not be so good next year.

It only takes about 15 to 20 minutes to shop around and review your PDP options, and it could save you literally hundreds of dollars and ensure you have the right coverage for your specific prescriptions.

The Bottom Line

Most Medicare agents are honest, hardworking professionals who want to help their clients, but the system is stacked against them when it comes to prescription drug plans. Between certification costs, compliance rules, and low commissions, many agents have chosen to focus on Medicare Supplements, Medicare Advantage plans, or other types of insurance products instead.

By learning how to shop for your own prescription drug coverage at Medicare.gov, you can take control of your health care costs, stay informed, and make sure you’re always getting the best prescription drug plan every year.

About the Author

As an independent Medicare Supplement insurance specialist, I work with all the major carriers throughout California, Nevada, and several other states. I shop around for my clients every year during their 60-day annual open enrollment period under the California Birthday Rule to help them save money on their Medicare Supplement premiums. Many of my clients have saved hundreds, even thousands of dollars on the same exact plan and coverage! Please click here to see what my clients have to say about my services.

There is no charge for my services as I’m compensated by the insurance carriers, not my clients. My goal is to help you find the lowest premiums and provide the best personal service possible—year after year. Unlike many agents, I won’t disappear after you sign up!

If you enjoyed this blog and found it helpful, please leave your comments, questions, or feedback below and feel free to share this article with your friends!

Thank you!

Ron Lewis Ron@RonLewisInsurance.com www.MedigapShopper.com (760) 525-5769 – Cell (866) 718-1600 – Toll-free

If you’re a Medicare Supplement (Medigap) policyholder living in California, there’s a little-known benefit that could save you hundreds (or even thousands) of dollars a year and many people don’t even know that it exists. It’s called the California Birthday Rule, and it gives you the right to switch your Medigap plan every year around your birthday, REGARDLESS OF YOUR HEALTH!

IMPORTANT: You can change your Medicare Supplement any time of the year, but if you do it around your birthday, it’s a lot easier because you don’t have to answer any health questions, there’s no medical underwriting, and YOU CAN’T BE TURNED DOWN FOR COVERAGE!

Medigap Plans Are Standardized

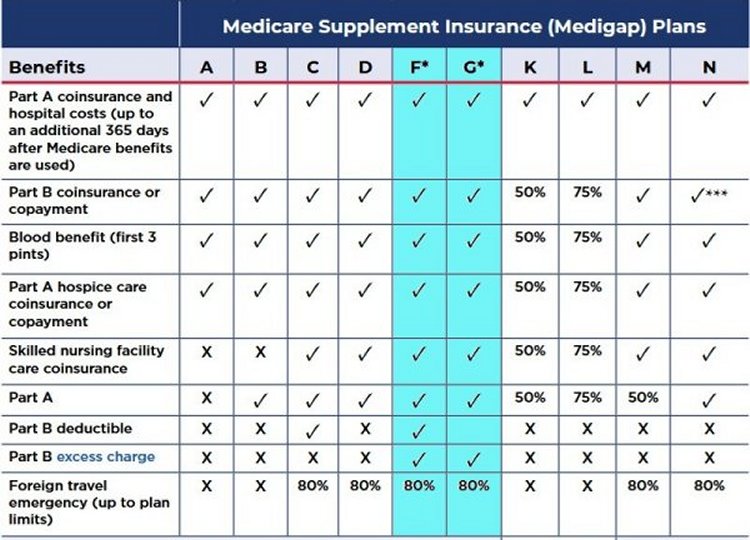

Nationwide, there are 10 standardized Medicare Supplement lettered plans to choose from, Plan A through Plan N. When I say “standardized,” that means that the coverage and benefits for every lettered plan are exactly the same regardless of what insurance carrier you sign up with. In other words, Plan G is Plan G, Plan N is Plan N, etc., regardless of what insurance carrier you are with. So it’s much easier to compare plans since every plan is exactly the same no matter which insurance carrier offers it.

NOTE:Technically, there are actually 12 standardized Medigap plans to choose from because there are high-deductible versions of Plan F and Plan G. In 2025, you will pay a $2,870 deductible before your coverage for either of these plans would begin.

As you can see, the only difference between Plan F and Plan G is the Medicare Part B deductible.

Which Medigap Plan is Best?

For those who are turning 65 or starting Medicare today, the best and most comprehensive Medigap plan is Plan G, which pays for everything except for the Medicare Part B deductible. The current annual Part B deductible (in 2025) is $257. That amount can change from year to year, but historically, it hasn’t changed by much.

Medicare Access and CHIP Reauthorization Act of 2015

Due to the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA), Medigap Plan C and Plan F were discontinued for new Medicare beneficiaries starting on January 1st, 2020. This legislation eliminated the availability of Medigap plans that cover the Medicare Part B deductible for individuals who became eligible for Medicare on or after that date. However, Plan C and Plan F are still available for people who were eligible for Medicare before 2020 or who already have one of those plans. They just aren’t available for those individuals that turned 65 or started Medicare on or after January 1st, 2020.

Let’s look at a common example of how switching under the Birthday Rule can save you money.

Why Plan G is More Popular Than Plan F

If you have a Plan F Medicare Supplement, you’re probably paying more than you need to. It’s usually much cheaper and more cost effective to switch to Plan G because both plans are identical in coverage except for the Medicare Part B deductible, which is $257 in 2025. Plan F covers that small deductible, while Plan G does not. That is the only difference between the two plans, yet the premiums for Plan F are usually significantly higher.

Even though Plan F covers that $257, it often costs $400–$1,000 more per year in premiums than Plan G, so in most cases, you’d save money by paying the lower monthly premium for Plan G and just covering that $257 deductible yourself.

IMPORTANT:If you can save more than $257 per year by switching from Plan F to Plan G, then Plan G is cheaper and more cost effective.

For example, if your Plan F premium is $250 per month and you can get Plan G for $200 per month, that’s a gross savings of $50 per month or $600 per year. If you pay the $257 on your own, your net savings will still be $343 per year ($600 – $257 = $343)! The Medicare Part B deductible is payable only one time per calendar year, so after you pay that small deductible, there is absolutely no difference between Plan F and Plan G for the remainder of the year!

NOTE: If you have Plan F and you switch to Plan G, if you’ve already met your $257 Part B deductible, you won’t pay it again until the following year since that small deductible is payable only one time per calendar year.

What Is the California Birthday Rule?

The California Birthday Rule is a special California state law that allows active Medigap policyholders in California to switch to a new Medigap plan with “equal or fewer” benefits every year around their birthday without medical underwriting during a 60-days following their birthday.

NOTE:In California, most carriers accept applications from 30 days before your birthday up to 60 days after your birthday, a 91-day window to switch Medigap plans without medical underwriting.

Most states don’t have a birthday rule, and if you develop a serious health condition, you could be stuck with your current health insurer and Medigap plan. But thanks to the California Birthday Rule, you have a guaranteed open enrollment period every year to shop around and save money on your premiums without worrying about being stuck or declined.

What Does Equal or Fewer Mean?

Again, under the birthday rule, you can switch to any Medigap plan that offers “equal or fewer” benefits than your current plan. In other words, you can switch from your current Medigap plan to any other Medigap plan that offers benefits that are the same or less comprehensive than what you currently have.

For example:

You cannot upgrade to a plan with more benefits (such as Plan N to Plan G).

You can switch to a plan with the same level of benefits (such as Plan G to another Plan G with a different carrier).

You can downgrade to a plan with fewer benefits (such as Plan F to Plan G, Plan G to Plan N, etc.).

This rule exists to prevent people from waiting until they are sick to “upgrade” to more generous coverage. However, it does give you freedom to shop around for lower prices on the same or lesser coverage without worrying about health questions or being declined.

Examples of “Equal or Fewer”

If you have Plan F, you can switch to Plan F with a different insurance carrier or to Plan G, Plan N, etc.

If you have Plan G, you can switch to Plan G with another insurance carrier or to Plan N, etc.

If you have Plan N, you can switch to Plan N with a different insurance carrier or to Plan A, etc.

Even if you’re not sure whether your current plan is the best deal, you can always switch to the same plan with a different insurance carrier during your birthday rule window, often saving hundreds and sometimes thousands of dollars per year without changing any of your benefits.

What States Have a Medigap Birthday Rule?

Today, more states are slowly adding their own birthday rules. Here is a current list of states that have a Medicare birthday rule:

California

Illinois

Idaho

Kentucky

Louisiana

Maryland

Nevada

Oklahoma

Oregon

Utah

Virginia

Wyoming

States with Year-Round Guaranteed Issue or Open Enrollment Rights

These states don’t have a Medicare birthday rule, but they offer year-round guaranteed issue or open enrollment periods without underwriting:

Connecticut

Maine

Missouri

New York

Washington

Do Most People Use the Birthday Rule?

Surprisingly, no! Many people don’t know this rule exists and they stay on overpriced Medigap plans for years thinking they’re stuck because of health issues, etc. If you take advantage of the birthday rule each year, you can keep your premiums under control and avoid being overcharged.

Rates Vary Significantly Between Insurance Carriers

As mentioned before, Medigap plans are “standardized” meaning that Plan G is Plan G, Plan N is Plan N, etc. The coverage and benefits for every Plan G, etc. are exactly the same regardless of what insurance carrier you are with. However, the rates between insurance carriers are not standardized. Every insurance carrier charges their own rates.

For example, right now in the 92024 zip code (San Diego), the Plan G rates for a 70 year old single female range from $217.78 to $319.79 per month! That’s a difference of $102.01 per month or $1,224.12 per year for the same identical plan and coverage!

NOTE:Several years ago, one of my clients, a husband and wife, moved to San Diego from Los Angeles. They were paying $809.00 per month for Plan G with United American, and I got them Plan G with Mutual of Omaha for $367.01 per month, which was a savings of $441.99 per month or $5,303.88 per year for the save identical plan and coverage! Rates are based primarily on age and zip code, and they are constantly changing. It‘s critically important to shop around every year!

How to Apply and Save Money!

To take advantage of the California birthday rule, you must do the following:

Live in California

Have an active Medigap plan

Switch to a Medigap plan with “equal or fewer” benefits

Apply during the 30 days before up to 60 days after your birthday

Email me at Ron@RonLewisInsurance.com or call me at 760.525.5769 (cell) or 866.718.1600 (toll-free) for a free quote or to switch plans

It only takes a few minutes to apply and there is never a charge for my service!

Conclusion

If you currently have a Medigap plan, you can change your plan every year around your birthday, REGARDLESS OF YOUR HEALTH! If you apply during your annual 60-day open enrollment period under the California Birthday Rule, YOU CANNOT BE TURNED DOWN FOR COVERAGE!

As an independent insurance agent specializing in Medicare Supplements, I work with all the major insurance carriers, not just one. (A “captive” insurance agent can only represent one insurance carrier.) I will do the shopping for you and find you the best rates, not just this year, but I shop around for all my clients every year around their birthday! The monthly premiums are exactly the same whether you let me do the shopping for you to save you money on your premiums or if you contact an insurance carrier directly! Please visit ClientTestimonials to read what some of my clients have to say about me.

Call, text, or email me today, and I’ll help you review your options in just a few minutes with no pressure or obligation. Let me help you save hundreds, or even thousands of dollars, on the exact same Medigap plan you already have. Won’t that be a nice birthday present?

If you liked this blog and found it informative, please click the “Like” button, and please send me your questions, comments, or feedback! And please feel free to share this article with your friends!

Thank you!

Ron Lewis Ron@RonLewisInsurance.com www.MedigapShopper.com (760) 525-5769 – Cell (866) 718-1600 – Toll-free

Medicare fraud is a serious issue that affects millions of Americans each year, and it costs taxpayers billions of dollars. Fraudulent activities not only waste valuable resources but can also put your personal health information at risk. This article takes a closer look at Medicare fraud, how to recognize it, and what you can do to protect yourself.

What is Medicare Fraud?

Medicare fraud occurs when someone intentionally misleads or deceives Medicare for financial gain. Here are some examples:

Billing for services you didn’t receive: Providers may bill Medicare for treatments, tests, or procedures that you didn’t actually receive.

Falsifying diagnoses or treatments: Some fraudulent providers might fabricate medical records to justify unnecessary treatments or prescriptions.

Unnecessary tests or treatments: Some providers might encourage you to undergo tests or treatments that are unnecessary, just so they can bill Medicare for them.

Medicare card theft: Fraudsters may steal your Medicare card to use it for unauthorized services or sell it to others.

How to Identify Medicare Fraud

It’s important to stay vigilant and be aware of potential fraud. Here are a few red flags to watch out for:

Unsolicited Calls or Visits: Be wary of phone calls or home visits from people who say they’re from Medicare or healthcare companies, especially if they are asking for your personal information. Medicare will never call you without reason to request personal information.

Offers of “Free” Services: If someone offers you “free” services in exchange for your Medicare number, that’s a huge red flag. While some services are covered by Medicare, be cautious about anything that sounds too good to be true.

Incorrect or Unfamiliar Charges: Always review your Medicare Summary Notice (MSN) or Explanation of Benefits (EOB). If you see charges for services you didn’t receive, contact the provider immediately.

Pressure to Join a Plan or Buy a Product: Scammers may pressure you to sign up for a plan or buy a product that you don’t need. Take your time to make decisions and consult with a trusted advisor if needed.

How to Protect Yourself From Medicare Fraud?

Here are some ways to protect yourself from Medicare Fraud:

Safeguard Your Medicare Number: Treat your Medicare card like a credit card. Don’t share it with anyone except your trusted healthcare providers.

Be Informed: Know what services and treatments are covered by your Medicare plan. Review your benefits regularly and ask questions if something doesn’t seem right.

Keep Track of Your Medical Bills: Stay organized by keeping records of your appointments, prescriptions, and any medical services you receive. This will make it easier to spot discrepancies on your billing statements.

Report Suspected Fraud: If you believe you’ve been a victim of Medicare fraud or notice suspicious activity, don’t hesitate to report it to:

Medicare: Call 1-800-MEDICARE (1-800-633-4227) or visit www.medicare.gov.

The Department of Health and Human Services Office of Inspector General (OIG): You can file a report online at oig.hhs.gov.

What Happens After Reporting?

Once a fraud case is reported, Medicare’s fraud prevention team will investigate the issue. If fraudulent activity is found, it could result in fines, loss of provider licenses, or even criminal charges against the perpetrator. Additionally, reporting helps Medicare improve fraud detection measures to protect other beneficiaries.

Final Thoughts

Medicare fraud is a real threat, but with awareness and vigilance, you can protect yourself and your healthcare benefits. Always question anything that seems suspicious and don’t hesitate to report anything unusual. Your attention to detail can help stop fraud and safeguard your Medicare benefits.

About Me

I hope that you have found this information to be interesting and informative. I’m an independent insurance agent with over 15 years of experience specializing in Medicare Supplement insurance, primarily in California. As an independent agent, I work with most of the major insurance carriers including Ace Property and Casualty, AFLAC, Mutual of Omaha, Cigna, Blue Shield of CA, Anthem Blue Cross, Health Net, Aetna, etc.

I have hundreds of clients, and I shop around for them every year. Please click here to see some of my client testimonials.

FINAL TIP: If you have any questions, or if you know anyone that is turning 65 or starting Medicare, or if you would like for me to shop around for you, I’m happy to help, and there is no charge for my service!!! Please feel free to call me or send me an email! Also, please feel free to forward this blog to anyone you know who may be interested.

The Annual Election Period (AEP) is from October 15th through December 7th each year. During this annual open enrollment period, you can sign up for or change your Medicare Advantage (MA) plan or your Prescription Drug Plan (PDP). Medicare Advantage and prescription drug plans are annual contracts, and they can change from year to year. Therefore, you should shop around and compare plans every year.

NOTE:If you have a Medicare Supplement, the AEP does not apply to you unless you want to enroll in or change your PDP.

If you have an MA plan and you want to change to a different MA plan, or if you want to leave your MA plan and switch back to Original Medicare, Part A (Hospital insurance) and Part B (Medical insurance), you would normally do so during the AEP. The new coverage will begin on January 1st of the following year. In most cases, you must stay enrolled in your MA plan for the calendar year beginning in January or on the date your coverage begins. However, in certain situations, you may be able to join, switch, or drop an MA plan during a Special Enrollment Period (SEP), such as if you move out of your plan’s service area, etc.

Pros and Cons – Medicare Supplements Versus Medicare Advantage Plans

When it comes to Medicare Advantage (MA) plans, I’m going to be totally honest and admit to you that I am biased because I don’t like them! Unless you can’t afford to pay the monthly premium for a Medicare Supplement (aka Medigap), I would NEVER recommend or advise someone to give up their Original Medicare rights (Part A and Part B) and sign up for an MA plan!

If you currently have an MA plan, or if you are thinking about signing up for one, I would strongly recommend that you read this article first so that you can make an “informed decision” about whether an MA plan is right for you and in your best interest.

There are pros and cons to each, but the benefits of having a Medicare Supplement plan far outweigh the benefits of having an MA plan. Please click here for a detailed comparison between Original Medicare and Medicare Advantage plans.

MA Plan Advantages

Here are some of the benefits of having an MA plan:

MA premiums can be very low, and some plans have no monthly premiums at all.

Some MA plans include Medicare prescription drug coverage (Part D).

Maximum out-of-pocket (OOP) costs are limited. Plans vary, but in 2025, the most you can pay for in-network OOP costs is $9,350 per calendar year. If you go out of network, you would normally pay all costs! (I wouldn’t really call this a benefit since $9,350 is a lot of money, and the most you would pay in OOP costs with a Plan G Medicare Supplement is the Medicare Part B deductible, which is currently $240 per calendar year in 2024! The Medicare Part B deductible for 2025 is projected to be $257. However, the Centers for Medicare & Medicaid Services (CMS) will not finalize the deductible until fall 2024.)

Some MA plans offer additional benefits such as vision, hearing, dental, and other health and wellness programs. (Some Medicare Supplement plans also offer additional benefits such as free gym memberships, vision, and hearing aid benefits.)

Medicare Supplement Plan Advantages

Here are some of the benefits of having a Medicare Supplement plan:

You have much more FREEDOM of choice with a Medicare Supplement than you do with an MA plan because you can go to ANY doctor, hospital, specialist, care facility, etc. in the United States as long as they accept Medicare, and most do, about 93%. (You can’t do that with an MA plan.)

You have much for financial stability with a Medicare Supplement than an MA plan because there are no unexpected expenses for deductibles, co-payments, hospitalizations, surgeries, chemotherapy, etc.

With a Plan G Medicare Supplement, other than your premiums, your maximum OOP cost in the 2025 calendar year will be no more than the Part B deductible, which is currently projected to be around $257. With an MA plan, your in-network maximum OOP “in-network” costs can be as high as $9,350! If you go out of network, your costs can be significantly higher.

NOTE:The Medicare Part B deductible is payable only one time per calendar year. If you’ve already met that deductible, you won’t have any other costs for Medicare-approved charges for the rest of the year.

You are not limited to a specific geographic region or a restrictive network of doctors, hospitals, specialists, care facilities, etc. like you are with an MA plan. Most MA plans are HMO’s and you will normally pay all costs if you go out of network.

With a Medicare Supplement, you can go directly to the specialist of your choice, ANYWHERE in the United States, as long as they accept Medicare. Most MA plans require you to go through a primary care doctor first and get permission to see a specialist within the local, geographic network.

Unlike MA plans, there are no HMO or PPO plans or networks with Medicare Supplements. You can go to any doctor or specialist in the US as long as they accept Medicare.

If you want to go to a renowned treatment center such as the MD Anderson Cancer Treatment Center in Texas, you can do so with any Medicare Supplement, as long as they accept Medicare. You can’t do that with most MA plans.

If you move to another part of the country, you can keep your Medicare Supplement, but you cannot keep your MA plan if you move out of your network.

There are only 10 “standardized” Medicare Supplement plans to choose from, (Plan A through Plan N). Since Medicare Supplements are standardized, the coverage and benefits for every Plan G, etc. is exactly the same with every insurance carrier, so it’s much easier to shop around and compare “apples with apples.” MA plans are not standardized, and the co-payments, deductibles, out of pocket costs, etc. vary between MA plans, and they change every year making them unnecessarily complicated and confusing.

A Medicare Supplement plan cannot be cancelled as long as you pay your premiums. MA plans are annual contracts, and they can be cancelled or benefits changed at the end of each calendar year.

There is no Annual Election Period (AEP) for Medicare Supplements, and you don’t have to shop around every year and make sure that your coverage, co-payments, co-insurance, deductibles, and benefits haven’t changed since the previous year. If there are any Medicare changes from one calendar year to the next, your Medicare Supplement will automatically pay the difference.

Medicare Supplements are “portable” meaning that you can keep them and take them with you if you travel to another state or if you move to another state, and your Medicare Supplement cannot be cancelled for leaving your “service area.” With most MA plans, if you travel outside of the MA plan’s service area for more than six months, you could be dis-enrolled from the plan.

With a Plan G Medicare Supplement, there are no co-payments when you go to the doctor. With most MA plans, you have to pay co-payments every time you see a doctor.

You can switch Medicare Supplement plans or Medicare insurance carriers any time of the year as long as you meet minimum health and underwriting requirements. With an MA plan, you can only join or leave an MA plan during the AEP or a SEP. Otherwise, you are locked into your MA plan for the entire calendar year.

NOTE:In California, there is a law called the California Birthday Rule. Under this law, if you have a Medicare Supplement, you can change it every year during the 60 days following your birthday to any other Medicare Supplement plan with “equal or fewer” benefits. For example, if you have Plan G, you can switch to Plan G with any other insurance carrier, regardless of your health. If you have Plan G, you can also switch to Plan N because Plan N has fewer benefits than Plan G, etc. Under the birthday rule, you just can’t switch from a plan with fewer benefits to greater benefits.

As you can see from the facts mentioned above, the benefits of having a Medicare Supplement far outweigh the benefits of having a Medicare Advantage plan.

Are Some Medicare Advantage Plans Really Free?

Because some MA plans have very low monthly premiums or no monthly premiums at all, some unscrupulous individuals promote them as “FREE” Medicare insurance plans, which is inaccurate, misleading, and, in my opinion, unethical. During the AEP, there are a lot of commercials for MA plans on TV. If you listen carefully, the one thing you’ll NEVER hear them mention is the maximum out-of-pocket costs for those plans. In 2025, in-network OOP costs can be as high as $9,350, and if you go out of network, you can pay significantly more!

Also, regardless of whether you have an MA plan or a Medicare Supplement plan, you still have to pay the monthly Medicare Part B premium, which is currently $174.70 per month for most people in 2024. The Medicare Part B premium in 2025 hasn’t been released yet, but it is estimated to be around $185.00 per month.

You Can Always Get a Medicare Advantage Plan But You Can’t Always Get a Medicare Supplement Plan

MA plans are adequate as long as you are healthy, but if your health should change and you develop a serious illness, you will wish that you had a Medicare Supplement instead of an MA plan because you will have much more freedom of choice and control over your health care with a Medicare Supplement!

Original Medicare (Part A and B) only cover about 80% of medical and hospital costs and Medicare Supplements pick up most of the remaining 20%. During the AEP, you can always switch from a Medicare Supplement to an MA plan, regardless of your health, and you can always switch from an MA plan back to Original Medicare (Part A and Part B), regardless of your health. However, if you switch back from an MA plan to Original Medicare during the AEP, there is no guarantee that you can get a Medicare Supplement as you must be in good health, answer health questions, and be medically underwritten to be approved. If you have any serious health issues, more than likely, you won’t be able to get a Medicare Supplement.

NOTE:There are some situations where you can switch from an MA plan to a Medicare Supplement as a “guaranteed issue” without answering any health questions or going through medical underwriting. If you are in this situation, please let me know.

Also, if you are in the first year of your MA plan, you are guaranteed the right to switch back to a Medicare Supplement during the first 12 months. This is called a trial right. The trial period gives you a year to try an MA plan and see if it’s right for you. If you decide it’s not, you are guaranteed the right to switch back to original Medicare (Parts A and B) and purchase a Medicare Supplement plan.

The Maximum Out of Pocket Cost for MA Plans Can Be Twice As Much As You Think

Depending on which MA plan you have, the most you would pay for in-network out-of-pocket (OOP) costs in 2025 is $9,350 per calendar year! If you go outside of your plan’s network, you will pay even more than that!

Now suppose that you get really sick and need expensive treatment in the second half of the year. You could end up paying up to $9,350 (or whatever your plan’s maximum OOP cost is) by the end of the calendar year, but your OOP maximum zeros out in January, and it starts all over again! You could potentially end up paying your OOP TWICE in a 12-month period!

Conclusion

If you have an MA plan, you give up your Original Medicare (Part A and Part B) rights and you compromise your freedom of choice to go to the best doctors, specialists, hospitals, care facilities, etc. throughout the United States. Unless you are impoverished and can’t afford to pay the monthly premium for a Medicare Supplement, I would never recommend an MA plan to a friend or family member as you are always better off with a Medicare Supplement.

I’m an independent insurance agent, not a captive agent, and I work with most of the major insurance carriers. I shop around for my clients, every year, and I will shop around for you too! If you have any questions or if you have an MA plan and would like for me to help you switch to a Medicare Supplement plan, please let me know! And if you have a Medicare Supplement, I’m happy to shop around for you to save you money on your premiums!

There’s no such thing as free Medicare insurance! As the old expression goes… “You get what you pay for!”

If you liked this blog and found it informative, please click the “Like” button, and please send me your questions, comments, or feedback! And please feel free to share this article with your friends!

Thank you!

Ron Lewis Ron@RonLewisInsurance.com www.MedigapShopper.com (760) 525-5769 – Cell (866) 718-1600 – Toll-free

If you are a California resident and you have a Medicare Supplement, aka a “Medigap” plan, I have good news for you! Under a law called the California Birthday Rule, you have 60 days of “open enrollment” following your birthday each year when you can change your Medigap plan, REGARDLESS OF YOUR HEALTH. During this period, there are no health questions to answer, no medical underwriting or waiting periods, and YOU CANNOT BE TURNED DOWN FOR COVERAGE! To qualify, the new plan must have “equal or fewer” benefits as your current policy.

For example, if you have Plan G, you can switch to Plan G with any other insurance carrier or you could switch to Plan N since Plan N has fewer benefits than Plan G. You just can’t switch from Plan N to Plan G, etc. under the birthday rule because Plan N has fewer benefits than Plan G.

NOTE:In California, most insurance carriers will let you apply during the 30 days before your birthday up to 60 days after your birthday, so in reality, you have a 90-day open enrollment period each year.

You can change your Medigap plan any time of the year, but if you do so around your birthday, it’s a lot easier because you don’t have to answer any health questions on the application and you can’t be turned down for coverage.

The Annual Election Period

There is another open enrollment period called the Annual Election Period (AEP) that goes from October 15th through December 7th every year. This open enrollment period has nothing to do with Medigap plans. It’s only for people with Medicare Advantage (MA) plans and/or Prescription Drug Plans (PDPs). If someone has an MA plan or a PDP, the AEP is the time to shop around and change those plans. The new coverage would begin on January 1st of the following year.

During the AEP, you can always switch from a Medigap plan to an MA plan, but there is no guarantee that you can switch from an MA plan to a Medigap plan. If someone has an MA plan, they are guaranteed the right to switch back to Original Medicare, which is Medicare Part A (Hospital insurance) and Part B (Medical insurance). However, they are not guaranteed the right to get a Medigap plan unless they are in a special enrollment period (SEP) that allows them to do so.

For example, if someone had an MA plan for the first time and they have had it for less than one year, they would be in a SEP, and they could still get a Medigap plan. Otherwise, they would have to answer health questions, be medically underwritten, and they could be turned down for certain types of health conditions.

NOTE:Medicare Part A and Part B cover approximately 80% of medical and hospital costs, so most people will get a Medigap plan to pick up most of the remaining 20% of the costs that are not covered by Medicare.

Most States Don’t Have a Birthday Rule

Most states don’t have a birthday rule, so the California Birthday Rule is definitely very beneficial for California residents because if your health should change, or if your rates go up significantly, or if you are not happy with your plan or insurance carrier, etc., you can always change to a different plan or insurance carrier, REGARDLESS OF YOUR HEALTH, every year around your birthday. In contrast, for those living in a state without a birthday rule, you could be stuck with your current Medigap plan, insurance carrier, high monthly premium, etc.

NOTE:Some states have recently added their own version of a birthday rule such as Idaho, Illinois, Louisiana, Maryland, Nevada, and Oregon. Besides the birthday rule, other states offer guaranteed issue protections for changing Medigap plans including Connecticut, Maine, Massachusetts, Missouri, New York, Rhode Island, and Washington. Each of these states have their own rules and requirements for changing Medigap plans, which are beyond the scope of this article.

When is the Best Time to Apply For New Coverage Under the California Birthday Rule?

In California, Medigap rates are based primarily on your age and zip code. Other factors that can affect the rate is if you use tobacco products and whether you live alone or with someone else in the household. Under the California Birthday Rule, most insurance carriers base their rates on your age after your birthday, but a couple carriers base their rates on your age on the date your application is submitted and signed. This one year age difference can make a big difference in the rate so for this reason, I normally recommend checking Medigap rates during the 30 days before your birthday each year.

Under the birthday rule, the new effective date is usually the 1st of the month following your birthday. For example, if your birthday is June 3rd, the new effective date would normally be July 1st, etc.

IMPORTANT:I shop around for my clients every year around their birthday to take advantage of the California Birthday Rule. If you aren’t a client of mine, and you would like for me to shop for you too, please let me know. As an independent agent, I work with all the major insurance carriers, and there’s no charge for my service!

10 Standardized Plans To Choose From

Nationwide, there are 10 standardized Medigap plans to choose from with lettered names, Plan A through Plan N. The term “standardized” means that the coverage and benefits for every Plan F, Plan G, Plan N, etc. are exactly the same no matter what carrier you are with. In other words, Plan G with Anthem Blue Cross is exactly the same as Plan G with Blue Shield of California, etc. Plan G is Plan G, Plan N is Plan N, Plan F is Plan F, etc.

As of January 1st, 2020, Medigap plans purchased by individuals who are turning 65 or who are new to Medicare can no longer cover the Part B deductible, which is currently $240 in 2024. (That amount can change from year to year.) Because of this, Plan C and Plan F aren’t available to people who are new to Medicare on or after January 1st, 2020.

NOTE:If you turned 65 before January 1st 2020 or you were eligible for Medicare before then, you can still get Plan F and Plan C. Those plans just aren’t available for those individuals who turned 65 after January 1st, 2020, etc.

Medigap Plans Are Standardized but Medigap Premiums Are Not Standardized

Although the coverage and benefits for all Medigap plans are standardized, the premiums for these plans are not standardized, and the rates vary significantly from one insurance carrier to another for the same identical plan and coverage.

For example, for a 72 year old female living in Encinitas, CA in the 92024 zip code, Plan G rates currently range from $178 to $280 per month for the same exact plan and coverage! That’s a difference of $102 per month or $1,224 per year! Since the monthly premiums vary significantly between insurance carriers, it’s important to shop around periodically.

The Application Process

Today, almost all Medigap insurance carriers in California use online applications that the agent completes. I work with clients throughout California and in several different states, so it’s not necessary to meet in person. The application process is simple, and it usually takes less than 15 minutes to complete.

In addition to the application, under the California Birthday Rule, most insurance carriers require some kind of proof that you currently have a Medigap plan. A copy of your Medicare Supplement card or a recent bill showing which plan you currently have (Plan G, etc.) is sufficient. Once the application has been submitted, the entire application process normally takes a couple of days to a week to complete since there is no medical underwriting. Underwritten applications usually take longer. After you are approved, you should contact your current Medigap insurance carrier to let them know that you will be canceling your old policy when your new policy begins.

CAUTION – Some Insurance Carriers Are Better Than Others!

In addition to finding an insurance carrier with competitive rates, you also have to be careful to choose a good insurance carrier because not all carriers are the same. Although the coverage and benefits for Medicare Supplement plans are standardized and the same, not all insurance carriers are the same; some are better than others!

For example, some insurance carriers will give you a 12-month rate lock and some don’t. Some have better financial ratings than others. Some will give you up to a 12% household discount if you live with someone else in your household, and some don’t. Some have much better customer service than others. Some have call centers in the US and some are overseas. Some provide free gym memberships and some don’t, etc. Price is important, but there are also other factors to consider when choosing a Medigap plan.

For More Information

As an independent insurance agent, I work with the major insurance carriers in California, Nevada, Arizona, and Washington state. I’m not limited to one particular insurance carrier. I shop around for my clients, every year, to find them the best rates, and I’m happy to shop for you too!

If you have any questions about the California Birthday Rule, etc. or if you would like a free, no-obligation Medicare Supplement quote, please don’t hesitate to let me know. There is no charge for my services as I am compensated by the insurance carriers, not my clients!

My contact information is below, and please click here to check out what my clients have to say about me. If you feel that the information in this blog would be helpful to a friend or family member, please feel free to pass it on and please feel free to add your comments below!