Over the past several years, Medicare Advantage (MA) plans have become very popular. Millions of Americans have enrolled in them, often because the plans advertise low premiums and extra benefits such as dental, vision, or gym memberships.

However, a growing number of seniors are discovering that MA plans are not always the best fit for their healthcare needs. In fact, many people eventually decide to leave MA plans and return to Original Medicare (Part A and Part B), often paired with a Medicare Supplement (Medigap) plan.

If you or someone you know currently has an MA plan, it may be helpful to understand why some seniors decide to switch back. The goal of this article is not to criticize MA plans, but rather to explain some of the most common reasons people reconsider their coverage after experiencing it firsthand.

Below are several key reasons why some seniors choose to leave MA plans.

1. Doctor and Hospital Networks Can Be Limiting

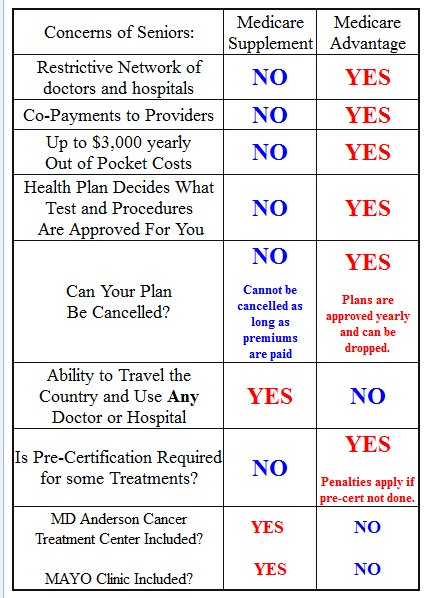

One of the biggest differences between MA plans and Original Medicare is the use of provider networks. Most MA plans are HMOs and some are PPOs. This means members typically must receive care from doctors and hospitals within the plan’s network in order to receive the lowest cost coverage. While some plans offer limited out-of-network benefits, they are often more expensive.

Many people don’t realize how restrictive these networks can be until they actually need medical care. For example, a doctor you have seen for years may not be included in the plan’s network. Even more frustrating, doctors and hospitals can leave networks from one year to the next, meaning your trusted provider may suddenly no longer be covered.

Original Medicare works very differently. Patients can generally see ANY doctor or hospital in the United States that accepts Medicare, which includes the vast majority of providers, approximately 93%. For seniors who value flexibility and freedom in choosing their healthcare providers, this can be a major advantage.

2. Prior Authorization Requirements

Another issue that sometimes surprises MA members is the requirement for prior authorization. Prior authorization means the insurance company must approve certain procedures, tests, or treatments before they are performed. While this process is intended to control costs and ensure appropriate care, it can sometimes lead to delays or complications. For example, a physician may recommend a particular diagnostic test or treatment, but the MA plan may require additional approval before the service is covered. In some cases, this can delay care while paperwork is reviewed.

Original Medicare generally does not require prior authorization for most medically necessary services. This can make the process of receiving care simpler and more straightforward for patients and their doctors.

3. Referrals to Specialists

Most MA plans require members to obtain referrals before seeing a specialist. This means that if you want to see a cardiologist, dermatologist, or other specialist, you may first need to visit your primary care physician and obtain a referral. While some people are comfortable with this system, others find it inconvenient.

With Original Medicare, referrals are typically not required. Patients can schedule appointments with specialists directly, provided the specialist accepts Medicare. For seniors who want greater control over their healthcare decisions, this difference can become an important factor.

4. Coverage When Traveling

Travel is another area where some MA members encounter unexpected limitations. Many MA plans are designed around regional networks. If you travel outside your local area for an extended period of time, you may find that accessing routine medical care becomes more complicated.

While emergency care is usually covered nationwide, non-emergency services may be limited to the plan’s network. Original Medicare, on the other hand, is accepted by doctors and hospitals across the country. This makes it much easier for retirees who travel frequently, spend part of the year in another state, or simply want peace of mind while away from home.

5. Costs Can Be Less Predictable

MA plans often advertise low monthly premiums, and in some cases the premium may even be zero. While this can sound very appealing, it’s important to look at the total potential cost of care.

Many MA plans require co-payments for services such as:

- Doctor visits

- Specialist visits

- Diagnostic tests

- Outpatient procedures

- Hospital stays

These costs can add up quickly if someone experiences serious health issues. In contrast, many people who choose Original Medicare also purchase a Medicare Supplement plan. These plans help cover many of the out-of-pocket expenses that Original Medicare does not pay, such as deductibles and coinsurance. As a result, healthcare costs can be more predictable from year to year.

6. MA Plans Have Maximum Out-of-Pocket Limits

Another factor many people overlook is the maximum out-of-pocket limit in MA plans. Each MA plan must set a maximum amount that a member could potentially pay during the calendar year for covered medical services. In 2026, that limit can be as high as $9,350 for in-network services, although some plans may set lower limits.

IMPORTANT: If you go out of network, you usually pay all costs!

While reaching that amount may not happen every year, it is possible if someone experiences a serious illness, hospitalization, or multiple medical procedures during the year. Also, if someone gets seriously ill in the last part of the year and they have met their annual deductible but are still requiring expensive care in the beginning of the following year, their annual deductible starts all over again every January, and they could potentially have to pay $9,350, etc. twice in a 12 month period!

By comparison, many people who combine Original Medicare with a comprehensive Medicare Supplement plan have much lower out-of-pocket exposure for Medicare-approved services. This can make healthcare costs far more predictable for retirees who want peace of mind. For example, with a Plan G Medicare Supplement, the maximum out-of-pocket cost for all of 2026 is the Medicare Part B deductible, which is only $283.

7. Switching Back Can Be Difficult Later

One of the most important facts many people don’t realize is that switching from MA to a Medicare Supplement plan later in life can sometimes be difficult.

When people first enroll in Medicare, they have a six-month Medicare Supplement open enrollment period. During this time, they can purchase any Medicare Supplement plan that they want without answering health questions. However, if someone decides to leave an MA plan later and apply for a Medicare Supplement plan, they are required to go through medical underwriting in most states. This means the insurance company can review health history and potentially decline coverage.

Because of this rule, some people feel “stuck” in their MA plan if their health has changed over time. There are a few exceptions in certain states that provide additional consumer protections, but the rules can vary significantly depending on where someone lives.

Making an Informed Decision

It is important to understand that both MA and Original Medicare with a Medicare Supplement plan can be appropriate depending on an individual’s preferences, budget, and healthcare needs.

Some people are perfectly happy with their MA plan and appreciate the additional benefits and lower premiums. Others prefer the flexibility and predictability offered by Original Medicare combined with a Medicare Supplement. The key is making an informed decision and understanding how the two types of coverage work before enrolling.

Final Thoughts

Healthcare coverage is one of the most important decisions people make during retirement. While MA plans work well for some individuals, others eventually decide that the flexibility and simplicity of Original Medicare better meets their needs.

If you have friends or family members enrolled in an MA plan who are experiencing frustrations with networks, referrals, or prior authorization requirements, it may be helpful for them to learn about the differences between these options. Everyone’s situation is unique, and the best coverage depends on personal circumstances. However, understanding how Medicare works can help seniors make confident decisions about their healthcare coverage for the future.

If you or someone you know currently has an MA plan and would like to better understand how it compares to Original Medicare with a Medicare Supplement plan, feel free to contact me. I’m an independent Medicare agent and I’m happy to help you review your options.

And if you found this article helpful, please feel free to share it with friends or family members who may have questions about their Medicare coverage.

Thank you!

Ron Lewis

CA agent #0B33674

NV agent #3822123

Ron@RonLewisInsurance.com

866.718.1600 (Toll-free)

760.525.5769 (Cell)

www.MedigapShopper.com

{kind=link}