This blog is a step by step guide explaining when to enroll, whether you can sign up by phone or online, and how to coordinate Medicare with a Medicare Supplement plan.

Turning 65 is an important milestone and for most Americans it means becoming eligible for Medicare. Many people turning 65 are surprised to learn that signing up for Medicare and choosing their coverage options involves several coordinated steps. Many people are unsure how to sign up, when to enroll, and which method is easiest. This blog explains the different ways to enroll in Medicare and which options work best depending on your situation.

Are You Automatically Enrolled in Medicare?

Some people are enrolled in Medicare automatically. You will usually be automatically enrolled in Original Medicare (Part A – Hospital insurance) and (Part B – Medical insurance) if you are already receiving Social Security retirement benefits at least four months before your 65th birthday.

If you are automatically enrolled:

- Your Medicare card usually arrives about three months before your 65th birthday.

- Coverage usually starts the first day of your birthday month (or the first day of the previous month if your birthday is on the 1st of the month).

- No Medicare application is required unless you want to delay Part B.

If you are not receiving Social Security benefits yet, you will need to apply for Medicare yourself.

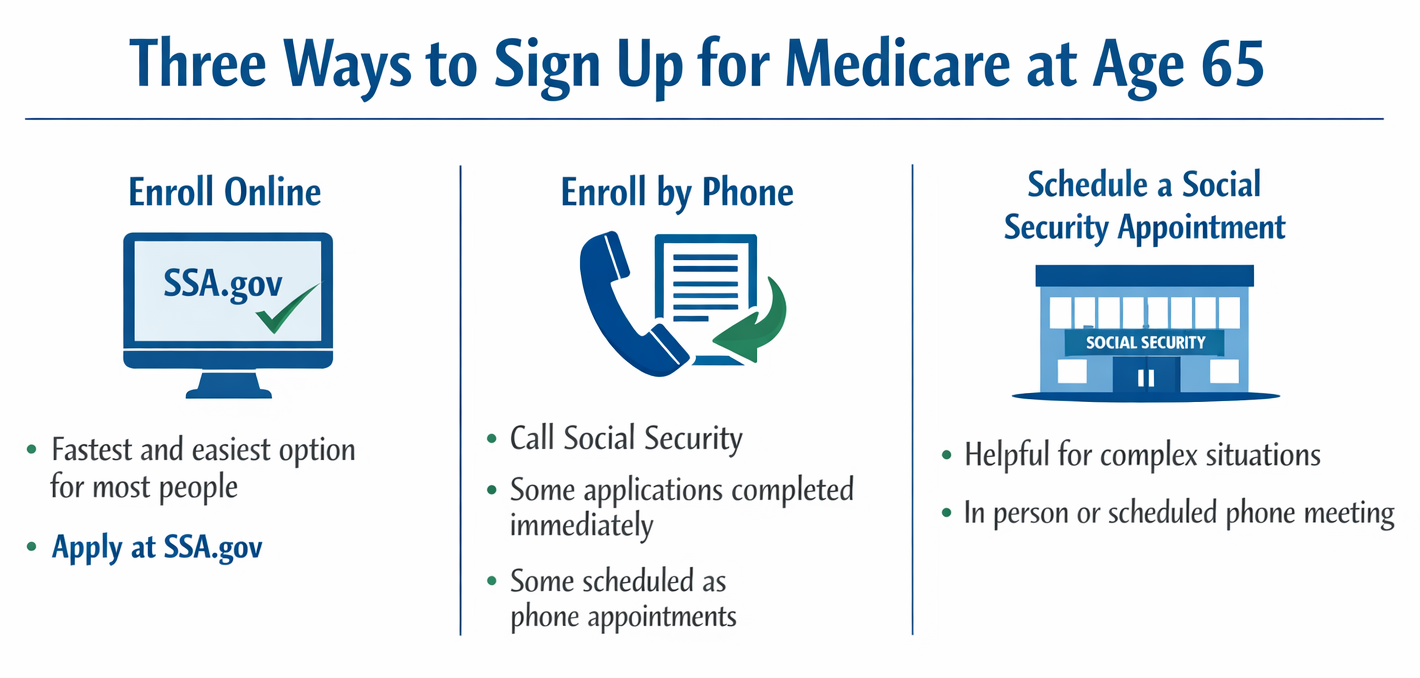

The Three Main Ways to Sign Up for Medicare

If you need to enroll yourself, there are three main options:

1. Enrolling Online Through the Social Security Website

For most people turning 65, enrolling online through the Social Security website is the fastest and easiest method. Please click here to enroll online.

NOTE: I know it seems counter-intuitive, but you go to the Social Security website, not the Medicare website, to sign up for Medicare.

Advantages of online enrollment include the following:

- Available twenty-four hours a day.

- No waiting on hold.

- Typically processed quickly.

- Often completed in about fifteen minutes.

Best for the following situations:

- People retiring at 65.

- Individuals not covered by employer insurance.

- Anyone comfortable using a computer.

- For most applicants, this is the best and simplest way to enroll.

2. Enrolling by Phone With Social Security

Many people prefer speaking with a representative. You can still enroll in Medicare by calling Social Security at (800) 772-1213.

Sometimes enrollment can be completed during the call. In other cases, Social Security schedules a follow up phone appointment with a specialist who completes the application with you.

Advantages of phone enrollment include the following:

- Helpful if you have questions.

- Useful for coordinating employer coverage with Medicare.

- Comfortable option for people who prefer personal assistance.

Best for the following situations:

- Applicants delaying Part B because they are still working.

- Individuals enrolling during a Special Enrollment Period.

- People who want guidance through the process.

3. Enrolling Through a Local Social Security Office

Some applicants prefer in person assistance. You can schedule an appointment with your local Social Security office to apply for Medicare. To set up an appointment, call Social Security at (800) 772-1213. Most offices now require appointments instead of walk in visits.

Advantages of in person enrollment include the following:

- Face to face support.

- Helpful for complicated situations.

- Useful if documentation is required.

Best for the following situations:

- Applicants with unique eligibility situations.

- Individuals who prefer meeting with someone directly.

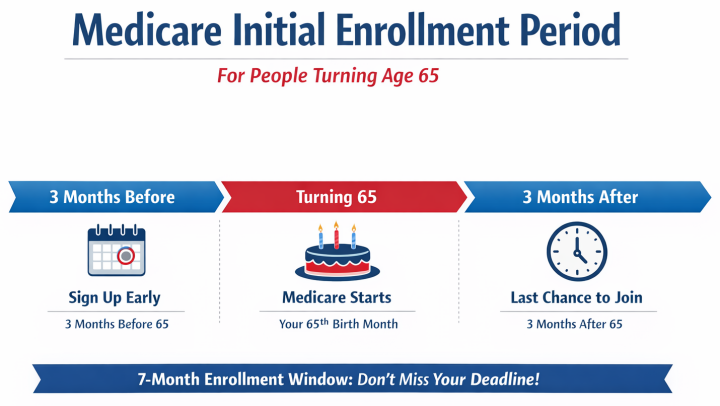

When Should You Apply for Medicare?

Your Initial Enrollment Period (IEP) lasts seven months:

- Three months before your 65th birthday month.

- Your birthday month.

- Three months after your birthday month.

Applying during the three months before your birthday month helps ensure your coverage starts on time.

What If You Are Still Working at Age 65?

If you or your spouse are still working and covered by employer health insurance, you may be able to delay Part B without penalty. This depends on the size of the employer and the type of coverage you have. Many people in this situation enroll in Part A (Hospital insurance) only and delay Part B (Medical insurance) until retirement. Before delaying Part B, it is important to confirm that your employer coverage qualifies. Please click here for more details.

NOTE: Part A is usually free, but the monthly premium for Part B is currently $202.90 for most people (in 2026), unless you are in a higher income bracket. If you are still working, you can usually defer paying the Part B premium until you leave your employer health plan.

Common Mistakes People Make When Signing Up for Medicare

Here are some common mistakes people make when signing up for Medicare:

- Waiting too long to apply and risking delayed coverage.

- Assuming enrollment happens automatically when it does not.

- Delaying Part B without confirming employer coverage rules.

- Missing the six month Medicare Supplement Open Enrollment window after Part B begins.

Avoiding these mistakes can save money and prevent future coverage problems.

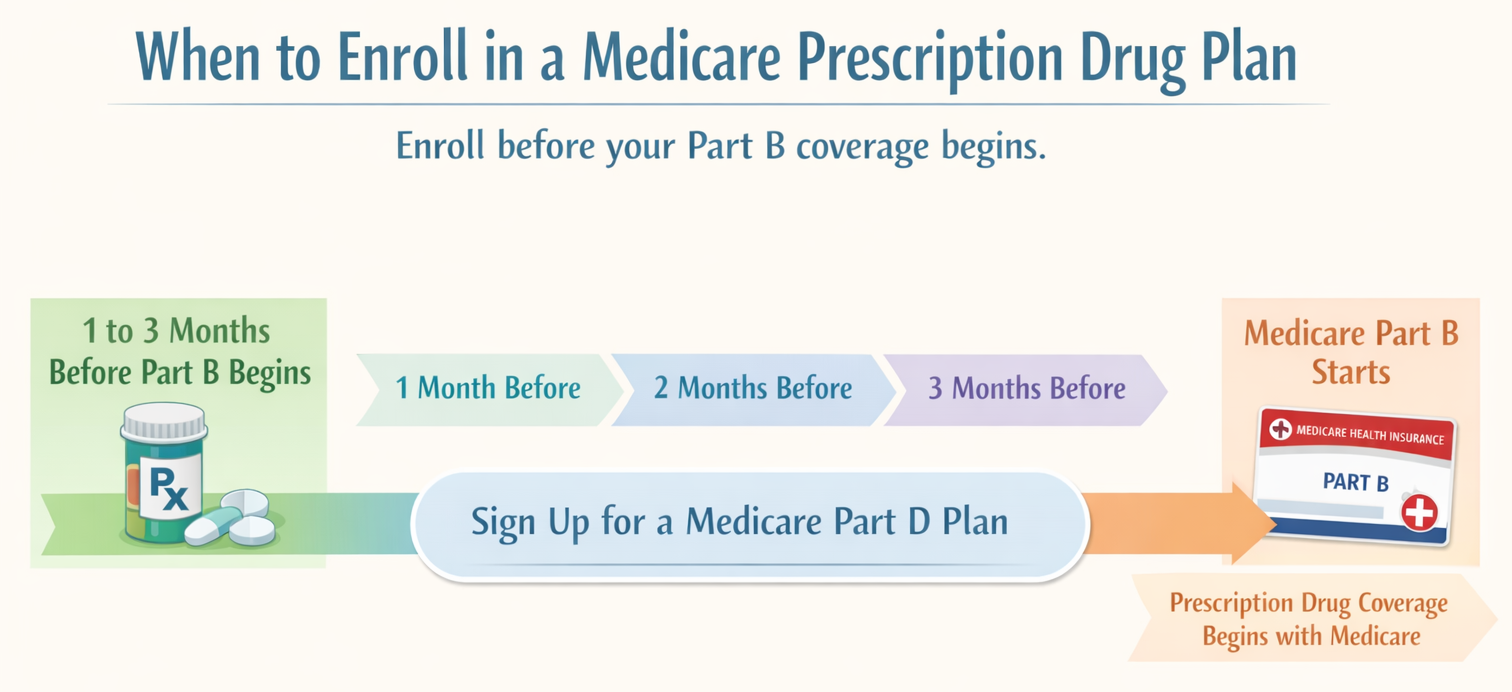

Do You Need to Enroll in a Medicare Part D Prescription Drug Plan?

When you first become eligible for Medicare, it is important to consider whether you should enroll in a Medicare Part D prescription drug plan. If you do not enroll in a Part D plan when you are first eligible and you do not have other creditable prescription drug coverage, you may have to pay a lifetime late enrollment penalty if you enroll later. Creditable prescription drug coverage usually includes employer or union coverage that is expected to pay at least as much as standard Medicare prescription drug coverage. It is important to confirm whether your existing coverage is considered creditable before deciding to delay Part D enrollment.

IMPORTANT: Even if you do not currently take prescriptions, enrolling in a low cost Part D plan when you first become eligible can help you avoid future penalties. In California, some Medicare Part D plans are available with a $0 monthly premium, which makes enrolling early an easy way for many people to avoid future penalties while keeping costs low.

It is also important to know that Medicare Supplement plans do not include prescription drug coverage. A separate Part D plan is needed if you want prescription coverage. Most people choose to enroll in a Part D plan when their Medicare Part B begins so their prescription coverage starts at the same time as their medical coverage.

The timeline below shows when to enroll in a Medicare Part D plan so your prescription coverage begins at the same time as Medicare.

How to Sign Up for a Medicare Prescription Drug Plan

Here are the most common ways to sign up for a Medicare Prescription Drug Plan:

Option 1: Enroll online (recommended)

Visit Medicare.gov and use the Plan Finder tool to compare all available Part D plans in your area. This allows you to review premiums, pharmacy networks, and estimated drug costs side-by-side so you can choose the plan that best fits your needs.

Click here to watch a short video I made that explains step-by-step how to sign up for a prescription drug plan.

Because many insurance agents are not appointed with every Part D carrier, and many agents no longer offer Part D enrollment assistance due to increasingly complex CMS compliance requirements, Medicare.gov is often the best place to make sure you’re seeing every available option.

Click here to read another blog I wrote explaining why you may be better off shopping for your own prescription drug plan instead of using an insurance agent.

Option 2: Enroll by phone

Call 1-800-MEDICARE (1-800-633-4227) and a Medicare representative can help you review your options and complete enrollment.

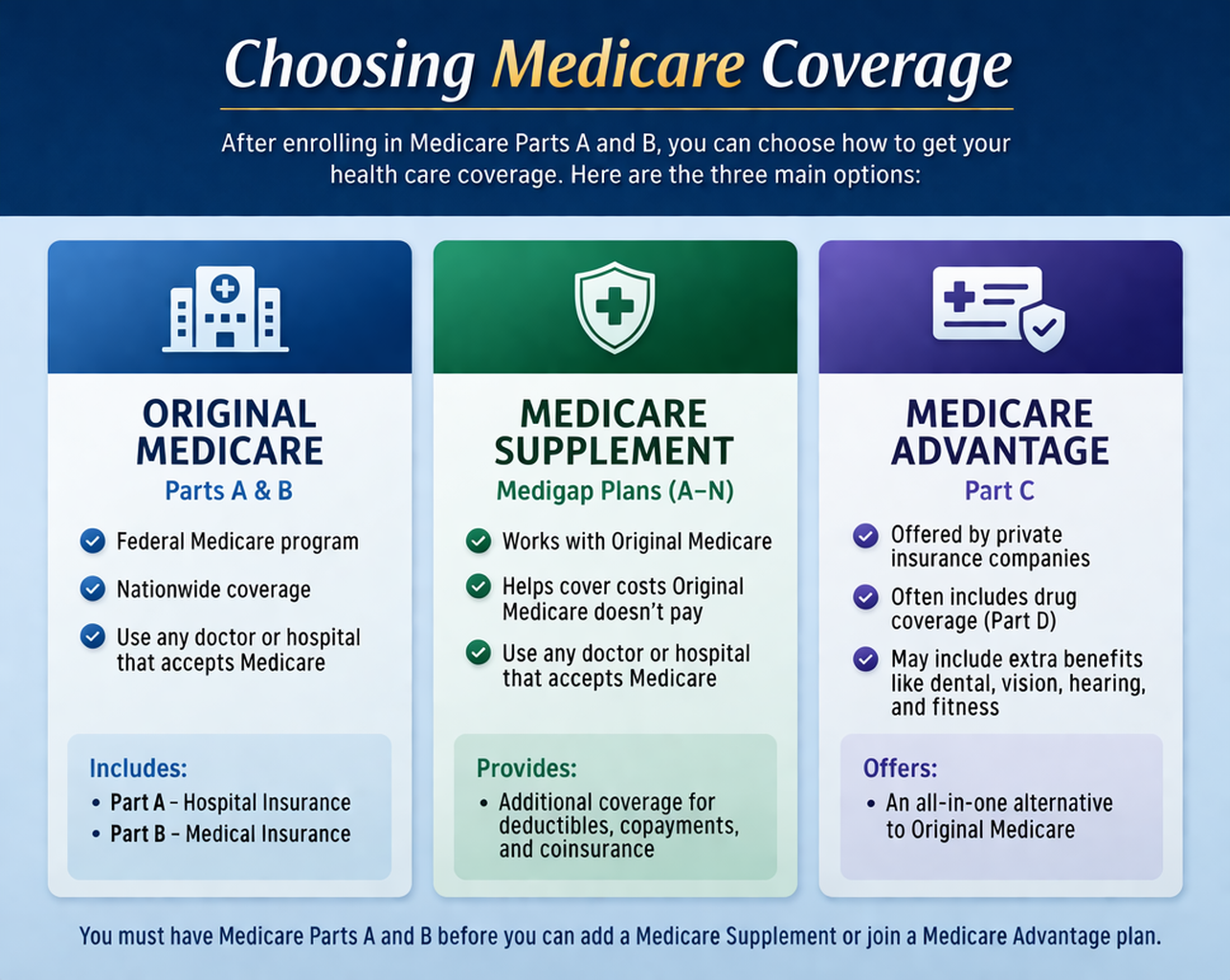

What Happens After You Enroll in Original Medicare?

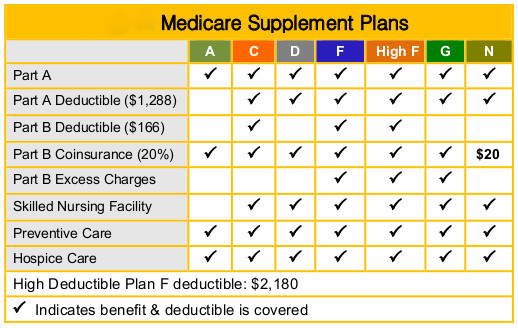

Once you are enrolled in Original Medicare (Part A and Part B), it’s important to understand that Original Medicare typically covers about 80% of approved medical expenses, and there is no limit on your out-of-pocket costs. Because of this, most people choose to add additional coverage.

Your main options include:

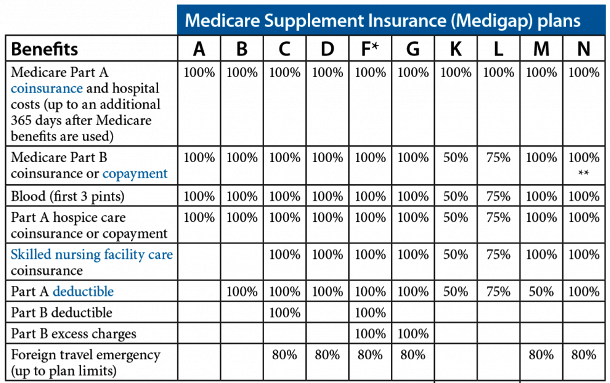

- A Medicare Supplement plan (also called Medigap)

- A Medicare Advantage plan

- A Part D prescription drug plan

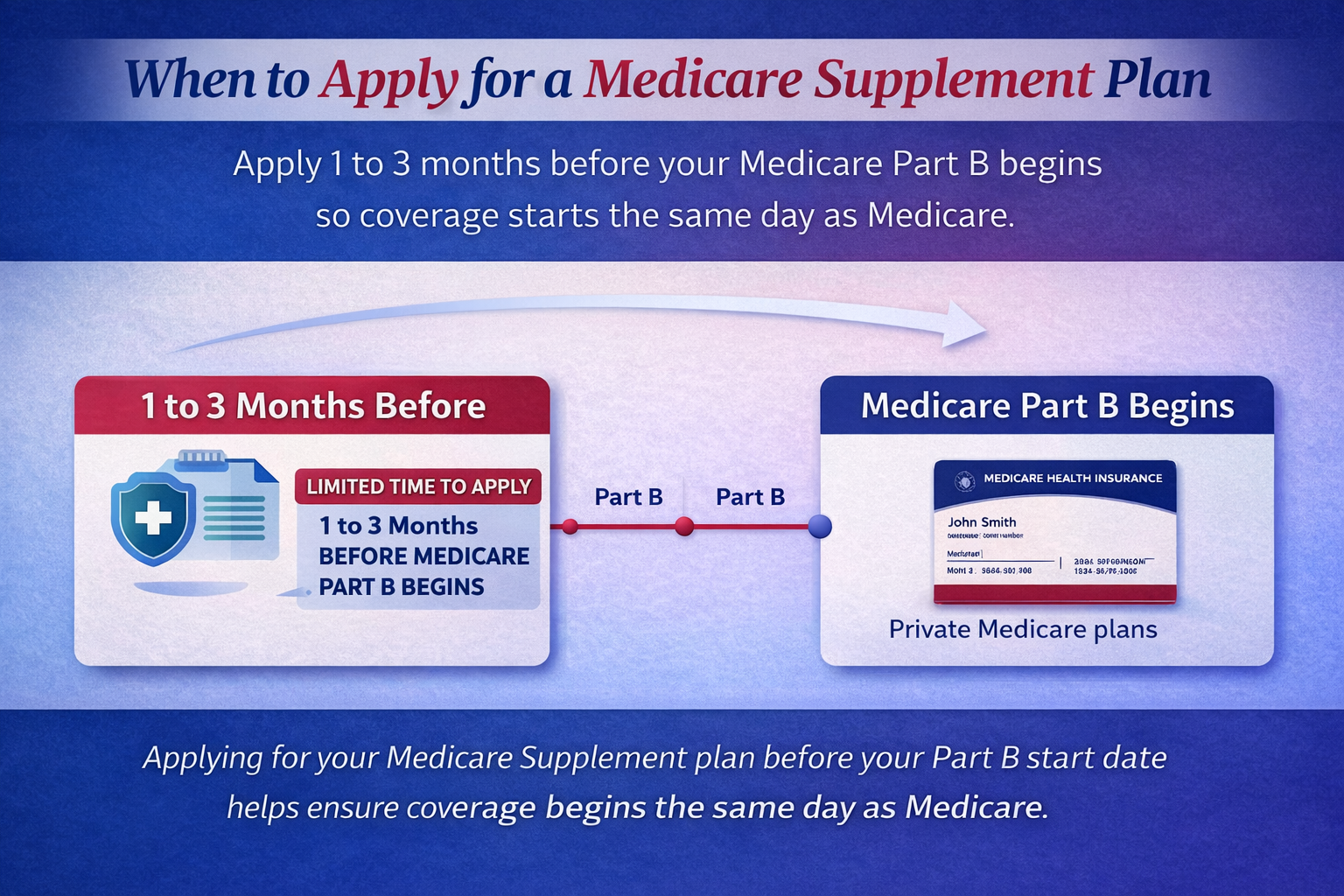

If you choose a Medicare Supplement plan, which many people prefer because it helps limit unexpected out-of-pocket costs, the best time to apply is before your Medicare Part B effective date so your coverage can begin the same day your Medicare coverage starts. Many people submit their Medicare Supplement application one to three months before their Part B start date to help avoid any gap in coverage.

Your six-month Medicare Supplement Open Enrollment Period begins when your Part B coverage starts. During this six-month window, you cannot be turned down or denied coverage due to health conditions. However, applying before your Part B effective date helps ensure your Medicare Supplement coverage starts on time.

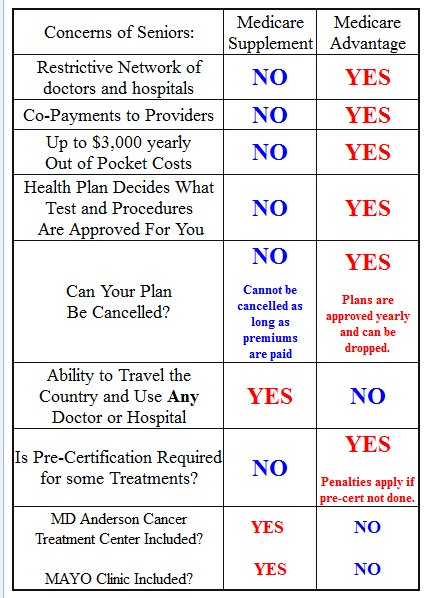

Some people choose a Medicare Advantage plan as an alternative way to receive their Medicare benefits. However, there are important differences between Medicare Advantage plans and Medicare Supplement plans.

Click here to read my article explaining why many people carefully compare these options before choosing a Medicare Advantage plan.

A Simple Checklist for Turning 65

- Find out whether you will be automatically enrolled.

- Decide whether you should delay Part B because of employer coverage.

- Choose whether to apply online, by phone, or through a Social Security appointment.

- Apply during the three months before your birthday month when possible.

- Review Medicare Supplement options once your Part B start date is confirmed.

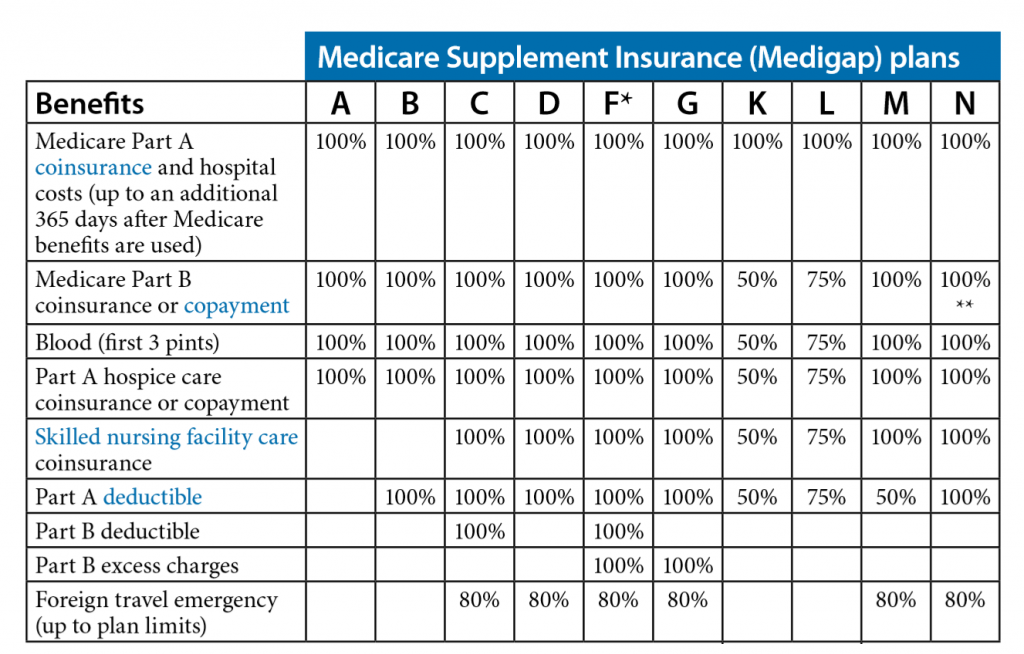

Understanding the Difference Between Enrolling in Medicare and Enrolling in a Medicare Supplement Plan

Signing up for Medicare and signing up for a Medicare Supplement plan are totally different. Enrolling in Medicare is done through Social Security and determines when your Part A and Part B coverage begin. Enrolling in a Medicare Supplement plan is done through a private insurance company using an insurance agent and helps cover most of the out of pocket costs that Original Medicare does not pay.

Many people assume these steps happen automatically together, but they do not. Coordinating the timing of your Medicare Supplement application with your Part B start date helps ensure your coverage begins the same day your Medicare coverage becomes active.

Medicare Supplements and Medicare Advantage Plans Are Totally Different

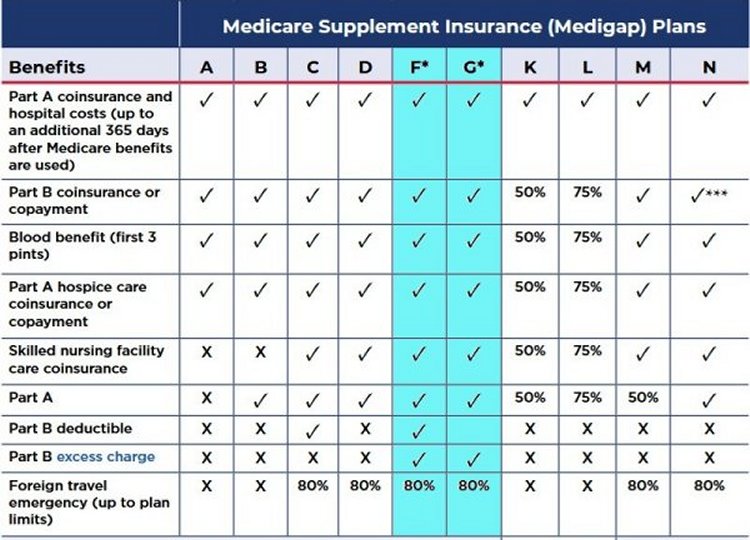

After enrolling in Medicare Part A and Part B, most people choose either a Medicare Supplement plan or a Medicare Advantage plan. These are two different types of coverage and they work in very different ways. A Medicare Supplement works alongside Original Medicare and helps pay most out of pocket costs such as deductibles and coinsurance. A Medicare Advantage plan replaces Original Medicare coverage with a private plan that includes provider networks and different cost structures. Most Medicare Advantage plans are HMOs and your choices are limited.

Understanding the difference between these options is an important step when planning your Medicare coverage.

A Medicare Supplement Insurance Specialist Helps Coordinate Your Start Date

One of the most helpful things a Medicare Supplement insurance specialist can do is coordinate the timing between your Medicare Part B effective date and your Medicare Supplement application. Submitting your Medicare Supplement application before your Part B start date helps ensure your coverage begins the same day your Medicare coverage becomes active. This helps prevent gaps in coverage and allows you to move into Medicare with confidence.

California Residents Have an Additional Medicare Supplement Advantage

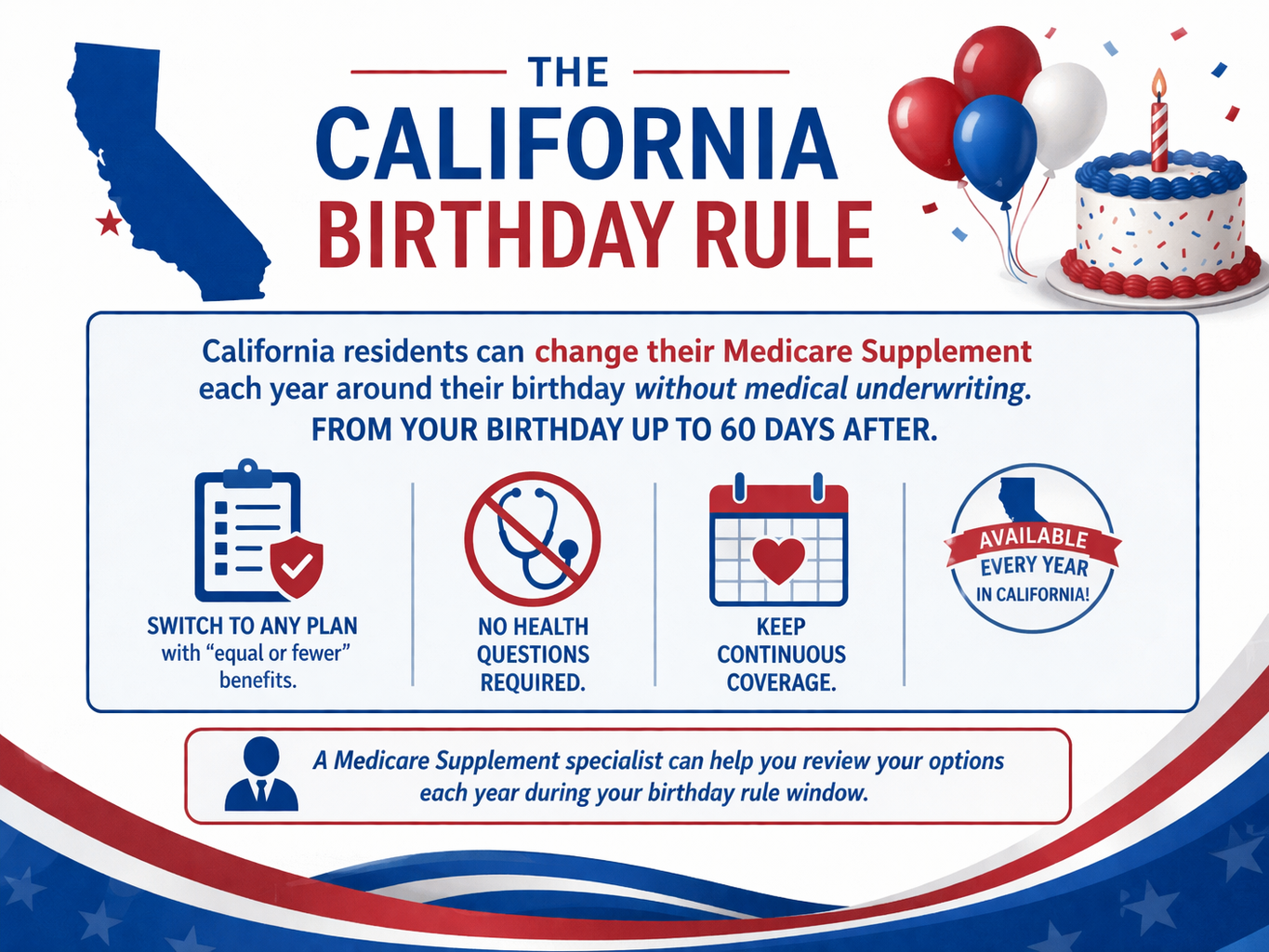

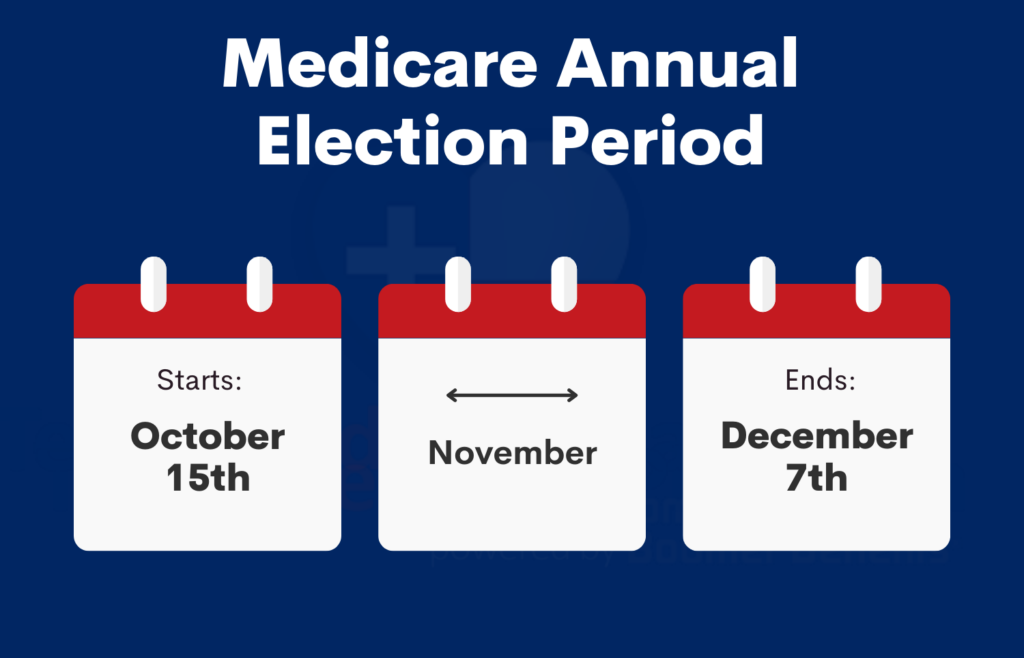

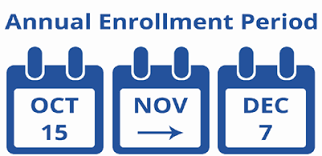

With a Medicare Advantage plan, you can generally only change your coverage during the Annual Election Period (AEP), which runs from October 15th through December 7th each year, unless you qualify for a Special Enrollment Period. Coverage selected during this time begins on January 1st of the following year.

With a Medicare Supplement, you can apply to change coverage at any time during the year. However, in most cases, you will need to answer health questions and go through medical underwriting.

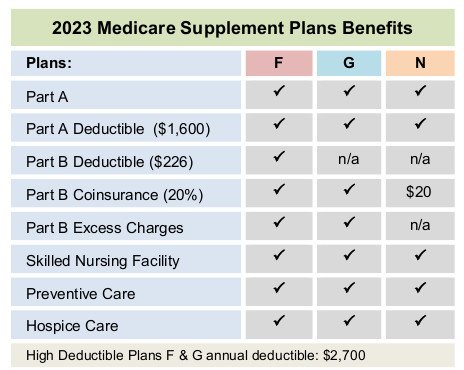

California residents have an added advantage under the California Birthday Rule. This law provides a 60-day window beginning on your birthday each year. During this time, you can switch to another Medicare Supplement plan with the “same or fewer” benefits without medical underwriting.

For example, if you have Plan G, you can switch to Plan G with any other insurance carrier, regardless of your health. In contrast, most states do not offer a birthday rule, which means individuals with health conditions may be unable to change plans or carriers without underwriting. If you are in California, it is a good idea to review your Medicare Supplement options around your birthday each year. I do this for my clients to help them take advantage of potential savings.

If you would like help reviewing your Medicare Supplement options or seeing if you may qualify for savings under the California Birthday Rule, I offer no cost consultations and would be happy to help you explore your options.

Final Thoughts

Signing up for Medicare does not have to be confusing. Understanding your enrollment options ahead of time helps ensure your coverage starts on time and helps you avoid unnecessary penalties or gaps in coverage.

If you are turning 65 soon and would like help coordinating your Medicare enrollment with a Medicare Supplement plan so your coverage begins on time, speaking with a licensed Medicare specialist can make the process much easier and more confident.

If you would like personalized help reviewing your Medicare Supplement options or timing your enrollment correctly, my contact information is below.

About the Author

I’m an independent Medicare Supplement insurance specialist working with most of the major insurance carriers throughout California, Nevada, and several other states. I help people turning 65 coordinate their Medicare enrollment so their Medicare Supplement and prescription drug coverage begin at the same time as Medicare.

I also work with many people who already have Medicare Supplement plans and would like to review their options. In California, the Medicare Supplement Birthday Rule allows policyholders to change their plans each year without medical underwriting, and I regularly help clients lower their premiums while keeping the same identical plan and coverage. Many of my clients have saved hundreds, and sometimes thousands, of dollars.

There is no charge for my services because I am compensated by the insurance carriers, not my clients. My goal is to help you find competitive premiums and provide dependable personal service year after year.

If you are turning 65 soon, or if you already have a Medicare Supplement plan and would like to review your options, I am happy to help.

You can also click here to read what my clients have to say about working with me.

Serving Medicare clients throughout California, Nevada, and several other states.

Ron Lewis

Ron@RonLewisInsurance.com

www.MedigapShopper.com

(760) 525-5769

(866) 718-1600

Congress passed this legislation to ensure that doctors would be paid adequately for providing Medicare services and to provide an incentive for doctors to continue accepting Medicare patients. Previous legislation had budgeted for doctors to have rate decreases over the years and there was concern that many doctors would stop accepting Medicare patients.

Congress passed this legislation to ensure that doctors would be paid adequately for providing Medicare services and to provide an incentive for doctors to continue accepting Medicare patients. Previous legislation had budgeted for doctors to have rate decreases over the years and there was concern that many doctors would stop accepting Medicare patients.